.svg)

.gif)

Introduction

This report was developed by OhBEV, an alcohol marketing agency working at the intersection of brand, data, and culture across wine, spirits, beer, and emerging beverage categories. We created this outlook to move beyond surface-level “trend lists” and provide decision-makers with a clear, experience-driven view of what is actually reshaping the gin market - from consumer behavior and pricing power to distribution dynamics, regulation, and climate risk.

The global gin market has experienced a dynamic decade of growth and change, evolving from a craft-fueled boom into a more mature and diversified landscape. Once defined by surging demand in traditional strongholds like the United Kingdom and Spain, the gin category is now at a crossroads entering 2026. Established markets are showing signs of saturation and even decline, while emerging regions and new consumer segments offer fresh avenues for growth. Premiumization - the shift toward higher-end, craft, and boutique gin products - has been a key driver in recent years, and gin’s versatility in cocktails has kept it in the spotlight of mixology trends. At the same time, heightened competition from other spirits (such as booming tequila and flavored whiskies), evolving consumer tastes, and regulatory hurdles are challenging gin brands to adapt and innovate.

In this long-form feature, we provide a comprehensive outlook for the gin market in 2026, examining global trends and forecasts, regional developments in key markets, the latest product innovations and emerging consumer trends, and strategies that gin brands can employ for success. The goal is to equip gin marketers and brand owners with expert insights - backed by data and industry analysis - to navigate the opportunities and challenges of the year ahead. From the enduring appeal of a classic London Dry to the rise of alcohol-free “spirits,” and from North America’s craft renaissance to Asia’s botanical experiments, we’ll explore how the gin market is shaping up in 2026 and what that means for stakeholders across the industry.

Global Gin Market Outlook: 2026 Trends and Forecast

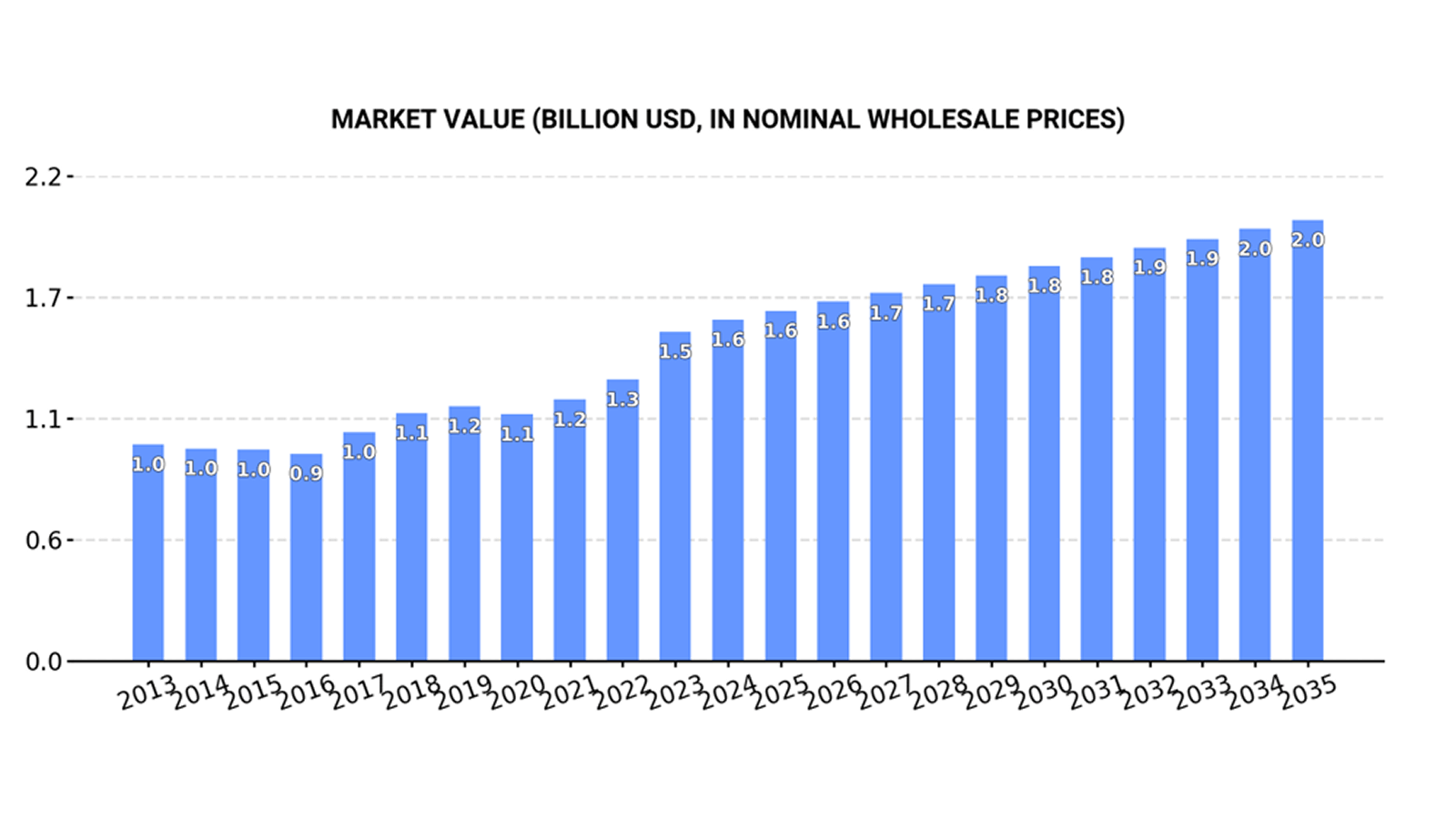

The worldwide gin market is projected to continue its expansion through 2026, albeit at a more moderate pace than the frenetic “ginaissance” of the late 2010s. According to a Technavio market outlook, the global gin sector is set to grow by approximately USD 6.68 billion between 2021 and 2026, which represents a compound annual growth rate (CAGR) of about 7.6% during this period. This growth will bring the total market size to an estimated low-$20 billions USD range by 2026. For context, Mordor Intelligence estimates the gin market at USD 23.4 billion in 2025, on track to reach roughly USD 29.5 billion by 2030 (around 4.7% CAGR). While methodologies differ, the consensus is that gin sales globally are trending upward, driven by premiumization and new markets, even as volumes in some mature regions level off.

Drivers of Growth

Several key factors are fueling the gin market’s growth into 2026. One major driver is the rising consumer demand for premium and super-premium gin products, as more people gravitate toward higher-quality spirits with craft credentials and unique botanicals. This premiumization trend has been a boon for revenue, as consumers are willing to pay more for upscale gin experiences. Additionally, the expansion of organized retail and online distribution is making gin more accessible in developing markets. Supermarkets, liquor store chains, and e-commerce platforms are dedicating more shelf space to gin, which boosts visibility and sales. Another growth driver is the cocktail renaissance and bar culture. Gin’s mixability has cemented its place in cocktail menus worldwide, from the classic gin and tonic to contemporary craft cocktails. The resurgence of cocktail culture - aided by trendy bars and at-home mixology - has increased on-trade consumption of gin in many cities.

Developing countries with rising disposable incomes are also contributing to global growth, as new middle-class consumers explore Western spirits like gin. Markets in Asia-Pacific, Africa, and Latin America are seeing heightened interest in gin, often starting with imported premium brands and gradually including local craft productions. Furthermore, innovation in flavors and botanicals has drawn in consumers who previously found gin too juniper-forward or bitter; a wave of flavoured gins (from fruit infusions to herbaceous blends) expanded gin’s appeal to new demographics during the last decade (more on this in the Innovations section). Finally, cultural trends such as premium gifting (gin gift sets, special editions) have given the category an additional push, especially around holidays and special occasions.

Global Market Trends

Despite overall growth, the gin market’s trajectory is a story of contrasts across different regions. Recent industry data shows that global gin volumes grew by only around 2% from 2023 to 2024, indicating that the era of double-digit surges is behind us. That modest global growth, however, masks stark regional variations. The world’s largest-volume gin market is not the UK or US as some might assume, but rather the Philippines, where a longstanding local gin culture has propelled consumption to staggering levels. The Philippines alone accounts for an outsized share of global gin sales by volume - roughly 22 million cases annually in recent years (over 40% of world gin volume) - thanks largely to a single dominant brand, Ginebra San Miguel. In fact, Ginebra San Miguel (a mass-market gin in the Philippines) sold over 42 million nine-liter cases in 2024, growing by 16% that year. This explosive volume growth in one market highlights how emerging economies can sway global figures.

India is another bright spot: now the world’s most populous country, India is witnessing a craft gin renaissance and rising premium spirits consumption. Industry forecasts peg India’s gin market value growth at about 7.4% CAGR from 2025 to 2032, signaling a huge opportunity as cocktail culture catches on. In contrast, many European and North American markets are flat or contracting in volume as the post-boom “normalization” sets in. The U.K., historically gin’s second home, saw total gin sales decline by double digits recently (more on that under Regional Outlook). The United States, while not experiencing a gin “bust” per se, has long had a stable gin consumption level that only lately shows pockets of growth in the higher-end segment.

Challenges Tempering Growth

Alongside these growth trends, the gin industry faces several challenges heading into 2026 that temper its expansion. One challenge is distribution and supply chain complexity, especially for smaller craft gin producers trying to reach a global audience. As Technavio notes, distribution hurdles can impede market growth - from logistical costs of shipping bottles internationally to securing shelf space in competitive retail environments. For instance, importers in key markets may face new tariffs or trade barriers that raise the cost of foreign gin. (In 2025, the U.S. introduced new import tariffs on spirits, adding 10-25% cost on gin from the UK and EU, which forced some brands to rethink pricing or scale back exports.) These kinds of trade policies can challenge gin brands to adapt quickly or risk losing market share to local alternatives.

Another headwind is the intensifying competition from other spirits categories. Over the past few years, spirits like tequila and mezcal, flavored whiskeys, and even premium rum have been capturing the imagination of consumers, occasionally at gin’s expense. The tequila category, for example, underwent a premium boom with celebrities and luxury positioning, and in the U.S. the super-premium tequila segment is about twice the size of gin’s in terms of market share. Gin now has to fight harder for attention as the “next new thing” amid a crowded field of drink options. Additionally, stringent regulations on alcoholic products remain a constant challenge. Regulations govern everything from production (minimum ABV and prescribed ingredients for something to be called “gin”) to labeling, marketing, and sale of spirits. In some countries, high alcohol taxes or advertising restrictions can stifle growth or favor local spirits over imports. Compliance costs and legal hurdles (such as obtaining distribution licenses, meeting label laws across jurisdictions, etc.) can be especially onerous for small gin companies.

Moreover, market saturation and consumer fatigue have become real issues in gin’s established heartlands. The gin boom of the 2010s led to a proliferation of brands - by 2020 the UK had over 560 distilleries, a record high, largely gin-driven. This crowded marketplace means brands struggle to stand out, and retailers have begun cutting back on the overabundance of similar products as growth cooled. Consumers, too, can feel overwhelmed by the sheer volume of gin choices, leading some to retreat to familiar classics rather than experiment endlessly. Finally, shifting consumer preferences toward health and wellness pose a subtle challenge: there’s a rising trend of mindful drinking (more low- and no-alcohol choices) which could limit alcohol consumption growth overall. While gin benefits from a low-calorie image relative to sugary drinks and has low/no-alcohol variants in the works, any broad movement toward reduced alcohol intake means spirit brands must adjust their strategies (we’ll discuss how in Innovations).

2026 Outlook in Summary

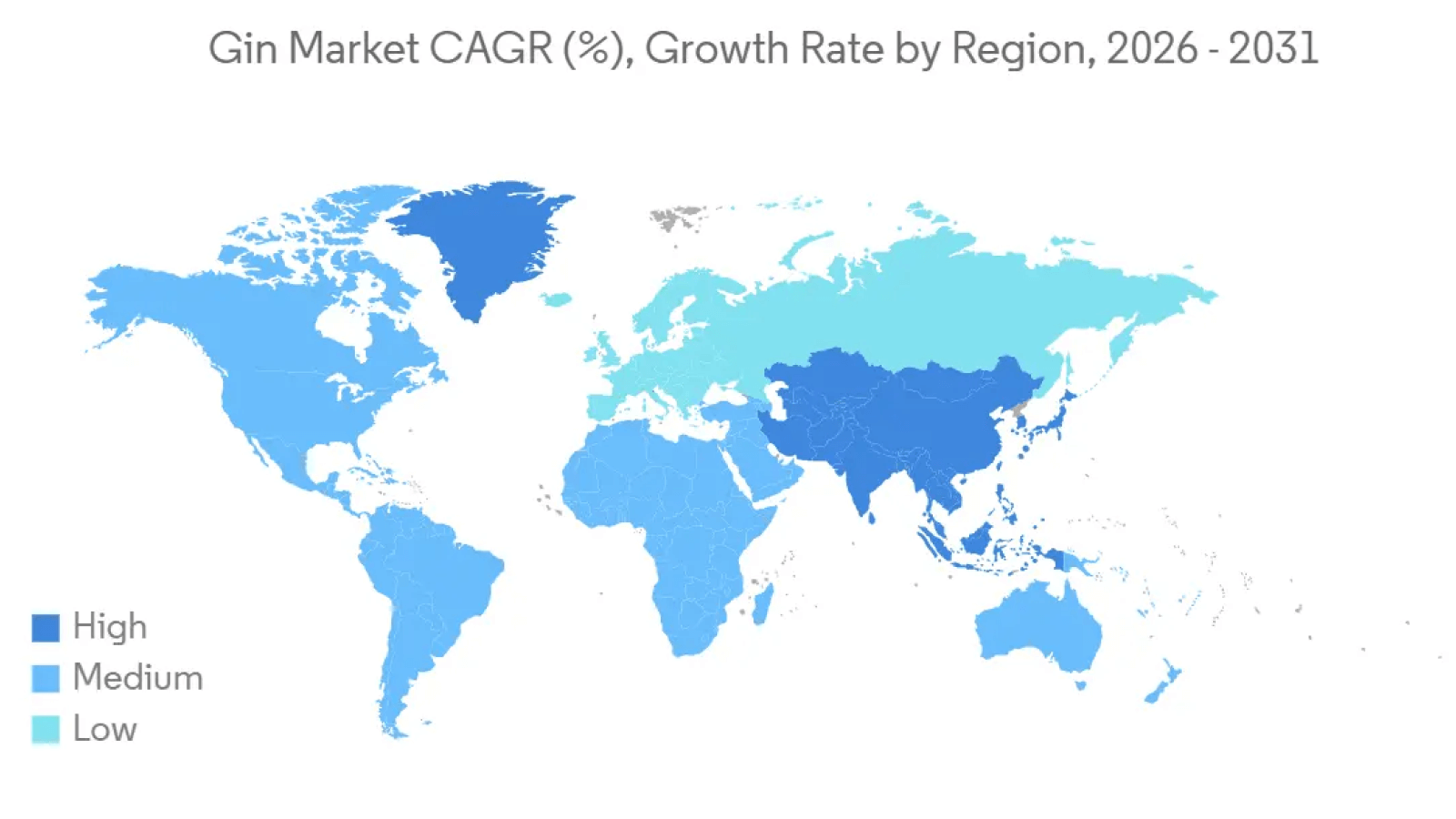

The net effect of these drivers and challenges is a gin market that, in 2026, is growing in value and evolving in character, but requires more strategic effort from participants than during the easy boom years. Global demand is forecast to rise modestly in volume and healthily in value, as premiumization lifts revenues. Europe is expected to account for the largest slice of market value and will contribute an estimated 43% of the market’s growth through 2026, even though its mature markets are slowing down. North America will remain a significant market with opportunities in the craft and super-premium niches. Asia-Pacific is poised for the fastest growth rate percentage-wise, thanks to rising interest in premium gin in countries like India, Japan, and beyond. In the following sections, we delve into regional outlooks to unpack these trends further, then explore how innovation is keeping gin relevant, and what strategies brands should adopt to thrive in 2026’s environment. Overall, the gin category is transitioning from a period of frenzied expansion to one of consolidation and refinement - where long-term success will favor brands that combine quality, authenticity, and agility in the face of changing market conditions.

Regional Outlook

While the global trends give a big-picture view, each region has its own story in the gin market’s 2026 outlook. Here we break down the regional dynamics and forecasts for North America, Europe, and Asia-Pacific, which represent the major arenas for gin’s future growth (or contraction). These regional snapshots highlight how local culture, economic factors, and consumer preferences shape the gin market, and they provide context for how brands can tailor their approaches in different parts of the world.

North America (USA & Canada)

In North America, the gin market presents a mixed picture of modest overall size but high potential in specific segments. The United States and Canada historically have not been as gin-obsessed as some European counterparts - vodka, whiskey, and tequila have long overshadowed gin in terms of mainstream popularity. However, recent years have seen renewed momentum in the premium and craft gin segment across the U.S. and Canada, suggesting that North America may be on the cusp of its own mini “gin renaissance” at the top end of the market.

United States

The U.S. is the largest economy and a trendsetter in cocktails, so its influence on the gin category is significant even if per-capita gin consumption is relatively low. For much of the past two decades, U.S. gin sales remained fairly flat, hovering around 10 million 9L cases per year. Gin was often regarded as a niche spirit - beloved by certain cocktail enthusiasts but overlooked by the broader public, many of whom favored the neutral smoothness of vodka or the familiarity of brown spirits. That said, signs point to a shift in U.S. gin consumption, especially in the super-premium tier. Over the last decade, the super-premium gin segment in the U.S. (think brands like Hendrick’s Orbium, Tanqueray No. Ten, and small-batch American craft gins) has grown nearly tenfold, albeit from a small base. By 2025, about 27% of U.S. gin sales by value were in the super-premium category, which indicates a sizable high-end market - though for comparison, in tequila the super-premium share is almost double that, showing gin still has room to premiumize further.

Notably, some leading premium gin brands have posted impressive gains: for example, Hendrick’s Gin’s U.S. sales jumped 10% in 2022 to over 587,000 cases. Such growth outpaced that of many other spirit categories; in fact, in the 2022 U.S. on-trade (bars/restaurants), gin’s sales growth outstripped whiskey, rum, and vodka, reflecting a rising interest in gin cocktails among American consumers. Gin is increasingly becoming a “must-have” spirit on cocktail menus, from classic Negronis and Martinis to creative new concoctions, signaling a cultural shift: more U.S. bartenders and patrons are embracing gin’s botanical complexity.

However, the U.S. market also comes with challenges that temper gin’s breakthrough. One issue is consumer education and perception. Many Americans remain less familiar with gin’s flavor profile - particularly the juniper-forward taste - and some hold outdated perceptions of gin as a harsh, old-fashioned spirit. As Alicia Johnson, a senior brand manager at a major spirits company, noted, the botanical ingredients in gin (juniper, coriander, citrus peel, etc.) are not flavors the average American grew up with, making gin somewhat intimidating to the uninitiated. Overcoming this means gin brands and mixologists often need to reintroduce the spirit in a friendly, accessible way (for instance, highlighting a fruity or floral gin in a simple cocktail to lure in a vodka drinker).

Another factor is that the U.S. market is highly competitive across spirits - with tequila, bourbon, and others enjoying significant buzz - so gin has to fight for attention. Indeed, overall U.S. gin volume has actually seen slight declines in recent years even as premium subsegments rise, indicating that lower-end gin consumption is dwindling (perhaps an effect of older generations aging out or switching preferences). The net effect: the U.S. gin category is bifurcated, with standard gin struggling, but an enthusiastic upswell in craft and upscale gin enthusiasm that is keeping the category alive and growing in value.

For gin marketers in the U.S., success in 2026 will likely hinge on a few strategies: continuing to educate consumers and demystify gin’s botanicals (through tastings, bartender advocacy, and marketing that explains what makes gin special), doubling down on cocktail culture integration (ensuring gin is prominently featured in bars and in home cocktail recipes), and leveraging the American penchant for local, authentic brands. Indeed, the U.S. craft distilling scene has exploded - hundreds of small distilleries from New York to California now produce gin, often using local ingredients and creative recipes. This craft movement is giving gin a more “homegrown” appeal. It also proved advantageous in the face of trade policy changes: when U.S. tariffs on European spirits raised costs for imported gin in 2025, many bars and retailers started giving more shelf space to domestic craft gins as cost-effective alternatives. American craft gin distillers emphasizing regional botanicals (e.g., California citrus or Appalachian juniper varieties) and unique stories found themselves gaining new visibility as import prices rose.

In short, the U.S. gin market of 2026 values quality, storytelling, and mixability, and while it may not return to volume growth without converting a new generation of gin drinkers, it offers substantial opportunities in the premium segment.

Canada

In Canada, gin trends often mirror the U.S. but on a smaller scale. Canadian consumers have similarly warmed to craft and premium gins in recent years. Major cities like Toronto, Vancouver, and Montreal boast local distilleries producing small-batch gins featuring indigenous botanicals (for example, Quebec gins using spruce tips, or British Columbia gins with Pacific Northwest herbs). One Canadian gin, Park Distillery’s Alpine Gin, famously uses glacier water from Banff National Park as a base - even donating part of proceeds to park conservation - to underscore its local purity appeal. This reflects a broader trend of “place-based” gin marketing that resonates well in Canada. Consumer interest in experiential spirits (where they know the origin and story) is high. The overall size of Canada’s gin market is relatively modest, but growing steadily; industry reports have noted an uptick in gin’s market share in Canada as younger consumers explore beyond vodka.

Like in the U.S., gin-based ready-to-drink beverages (e.g., canned gin and tonics) have found a foothold for their convenience and trendiness. One difference in Canada is the provincial liquor board system - government-run liquor stores dominate distribution - which means a craft gin can gain wide provincial distribution if it passes the board’s criteria, sometimes giving local brands a strong boost. Canadian gin sales also get a seasonal bump in summer, when gin cocktails and G&Ts are especially popular in warm weather. For 2026, Canadian gin brands will likely continue focusing on craft authenticity and local pride, while import brands will emphasize quality and heritage to justify their premium positioning in a market with high alcohol taxes. Overall, North America’s outlook sees slow but steady growth in gin demand, concentrated at the premium end and propelled by cocktail culture. The challenge will be converting more casual drinkers to gin without losing the core base that appreciates its distinctive taste.

Europe (UK & EU)

Europe has long been the epicenter of the gin world - home to gin’s historical origins and many of its top brands, as well as some of the most enthusiastic gin-consuming populations. As we approach 2026, Europe remains the largest region for gin by market value, but it is also where the category’s recent growing pains are most evident. The narrative for Europe’s gin market is one of a boom that has leveled off: after a meteoric rise in the 2010s, growth has stalled and even reversed in key countries, forcing brands to adapt to a more mature, competitive environment.

United Kingdom

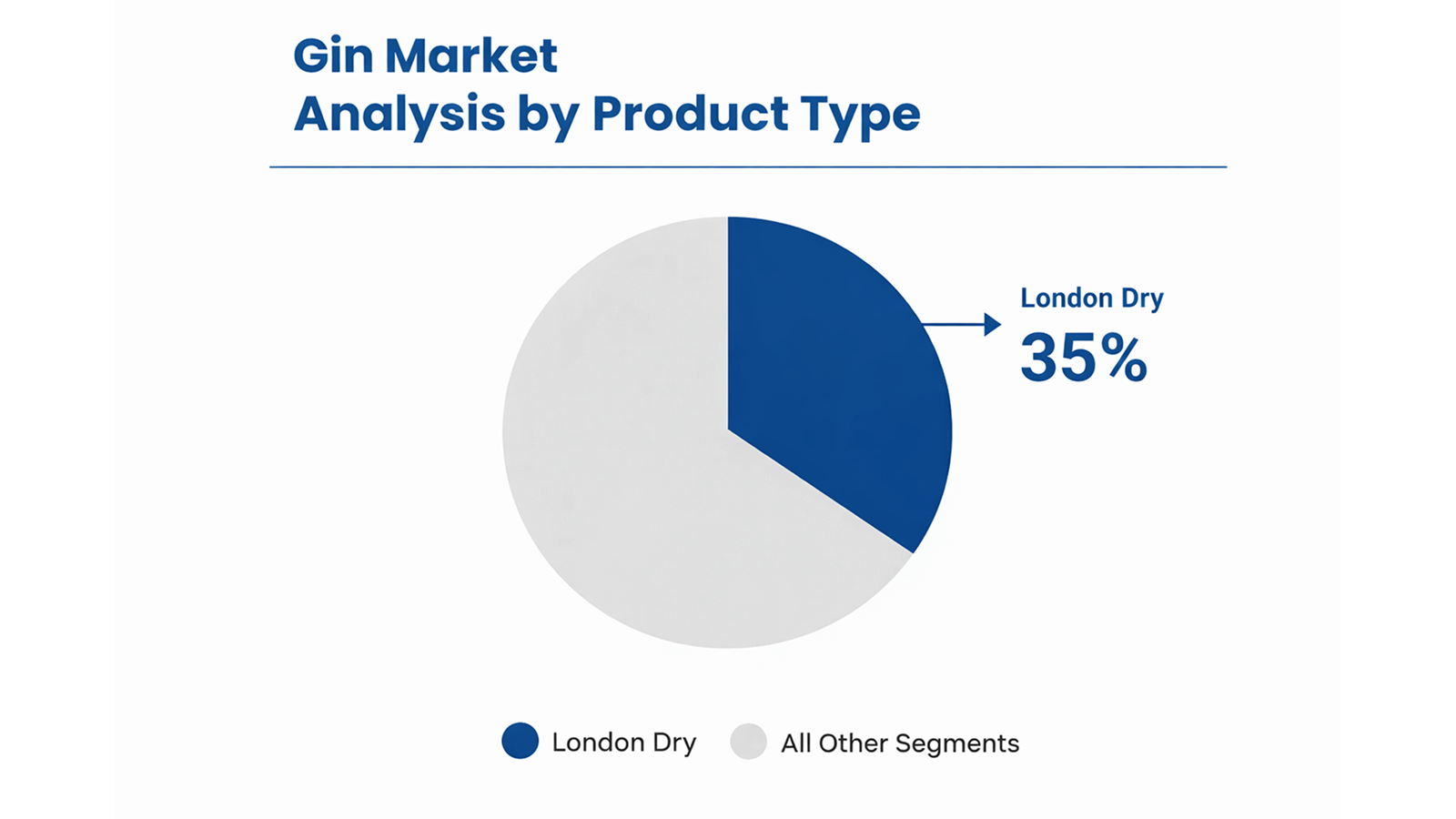

The UK deserves special attention, as it spearheaded the “ginaissance” and is still often considered gin’s spiritual home (even though gin was technically invented in the Low Countries). In the early- to mid-2010s, the UK experienced remarkable growth in gin demand - from craft distilleries popping up nationwide (enabled by a 2009 law change that made it easier to distill) to an explosion of new flavors and pink gins that attracted younger audiences. Between 2013 and 2019, premium gin sales in the UK soared, with double-digit annual growth rates at the height of the craze. By 2018, the number of distilleries in England surpassed those in Scotland (traditionally whisky territory), and by 2020 the UK had a record 563 registered distilleries, largely thanks to the gin boom. The COVID-19 pandemic even gave a temporary boost - during lockdowns in 2020, UK consumers experimented with at-home cocktails, pushing gin sales (especially flavoured gins) to new peaks. Flavored gins - from rhubarb to orange blossom to novelty color-changing gins - were at one point more than 30% of the UK gin category’s volume in 2020, indicating how much new entrants had expanded the category beyond traditional London Dry.

However, the past couple of years have seen a sharp reversal. Post-2021, as normal life resumed and the novelty wore off, the UK gin market began contracting. In 2023, premium-and-above gin volumes in the UK fell by a striking 16% year-on-year. The latest forecasts from IWSR and other analysts project a continued decline with a negative CAGR around -5% for 2023 through 2028 in the UK’s premium gin segment. Even total gin (all price tiers) is declining; Drinks International reports that between 2023 and 2024, UK gin volume dropped 13% - the steepest drop among major spirits categories in Britain, outpacing declines in vodka or whisky. What caused this dramatic downturn after years of abundance? A few factors are at play:

- Market Saturation and “Gin Fatigue”: The UK market became oversaturated with gin brands and line extensions. At one point, every supermarket, celebrity, and farm shop seemed to launch a gin. As a result, retail shelves and bar back-bars were crammed with dozens upon dozens of gins. When consumer demand stopped growing at the same pace, something had to give. Retailers have since rationalized their offerings, cutting back on weaker-selling labels. Consumers, too, felt “gin fatigue” - overwhelmed by choice and perhaps a bit jaded by gimmicky launches, many have retrenched to buying their established favorites. As Sipsmith co-founder Sam Galsworthy put it regarding the UK contraction, “the tide is retreating, and a receding tide takes ships with it”, meaning even some good brands are suffering simply because overall demand ebbed.

- Flavored Gin Fad Cooling: The UK’s love affair with sweet and flavored gins has cooled significantly. Those candy-colored pink gins and novel flavors that once drove growth are now leading the decline. Data indicates flavored gins in the UK are declining at more than twice the rate of traditional gins. Essentially, many who jumped on the pink gin trend may have been transient consumers; as tastes evolve, a chunk of these buyers have exited the category or moved to other drinks (for instance, some have shifted to flavored vodka or ready-to-drink cocktails). Meanwhile, the remaining gin aficionados have shown a renewed interest in classic styles. Producers report that consumers are “settling on their favorites” - often high-quality London Dry gins or classic distilled gins without heavy flavoring or sweetening. In other words, the boom educated a broad audience about gin, and now that the experimentation phase is over, many people discovered they actually prefer the taste of a juniper-forward, crisp gin. This return to the classics is positive for legacy brands and any newer brand that offers a refined, authentic gin profile.

- Economic and Regulatory Factors: The UK also had economic headwinds – rising inflation and an alcohol duty increase in 2023 made gin (especially premium bottles) more expensive for consumers, dampening sales. Furthermore, post-Brexit trade complexities and tariffs affected some international sales, although local consumption is the bigger issue. On the regulatory side, the UK maintains strict definitions for gin categories (London Dry, etc.), but that mostly affects production method rather than demand. However, new lower-alcohol products might face different tax categories, influencing how gin alternatives are marketed (more under Challenges).

Despite the current downturn, gin is far from dead in Britain. It’s arguably resetting to a more sustainable level. Gin still holds cultural cachet - witness the persistence of gin menus in pubs and the popularity of events like gin festivals or distillery tours. Looking into 2026, we expect the UK gin market to stabilize at a slightly lower volume, with a focus on quality over quantity. The brands likely to thrive are those with strong identities and loyal followings, or those tapping into the new consumer ethos of “less but better.” As one distiller, Nikolas Fordham of Ramsbury, observed, UK consumers now “want to know how and where their gin is made, and whether the brand aligns with their values”, not just grab any flashy new bottle. Sustainability, transparency, and heritage are becoming key selling points (for example, distilleries highlighting local ingredients or eco-friendly practices to appeal to gin lovers who have plenty of choices).

Additionally, innovation isn’t off the table - but it’s more subtle now. Instead of churning out another sweet flavor, UK gin brands are innovating with things like limited editions that have an interesting backstory or unique botanical twist, released in a controlled way to spark interest without flooding the market. In summary, the UK in 2026 will see a gin market in consolidation, with fewer, stronger players and a consumer base that’s more discerning but still passionate about the spirit.

Rest of Europe (EU)

On the continent, gin’s trajectory varies by country, but many echo the UK’s pattern to some degree. Spain, which was a gin hotspot (thanks to the gin-tonic craze of the early 2010s served in big “copa” glasses), has similarly hit a plateau. After years of growth, Spanish gin sales have contracted - premium gin volumes in Spain fell about 16% in 2023, matching the UK’s rate of decline. Forecasts for Spain also predict roughly -5% CAGR from 2023 to 2028 in the high-end gin segment. It appears Spanish consumers, like the British, moved on from the gin-tonic boom; even record tourism in Spain in 2023 didn’t fully reinvigorate gin demand, suggesting locals and visitors alike have diversified their drink choices.

Elsewhere in Europe, trends are a bit more mixed. Germany and France have seen slower, steadier gin growth historically (never as crazy as the UK/Spain boom, but still positive). Germany, for example, has a notable craft gin movement (e.g., Monkey 47 gin gained international fame), yet overall consumption growth was around only 1-2% annually mid-decade. Gin has a smaller niche in countries like Italy (where aperitifs and amaro liqueurs are culturally bigger) and Eastern Europe, but even there, urban cocktail bars have embraced gin for classics like Negronis and Martinis. The Netherlands and Belgium maintain a legacy with genever (the juniper spirit precursor to gin), but modern gin is popular among younger consumers in those markets too. One European market that stands out with continued enthusiasm is the Republic of Ireland, where gin saw a big uptick in the late 2010s and, despite some leveling off, remains a trendy spirit supported by local craft distillers and bars.

A pan-European factor is that Europe leads in gin innovation and brand variety. Many of the world’s top gin brands are based in Europe - from UK’s Gordon’s, Beefeater and Tanqueray, to France’s Citadelle, to Spain’s Larios, to Dutch Bols Genever. This means Europe is an exporter of gin culture worldwide. It also means competition within Europe is fierce. As growth slows, we may see more consolidation: big companies acquiring smaller gin brands (as was the case when Bacardi acquired Bombay Sapphire years ago, or more recently when spirits giants bought up craft distillers like Sipsmith and Monkey 47). Europe’s share of the global gin market by value is still substantial - nearly half of incremental growth through 2026 is expected to come from Europe - largely because of the value base (premium gins are priced higher in Europe than in many other regions and European consumers still buy a lot of them). But volume-wise, Europe might not contribute much growth; instead, value growth may come from a trading-up effect (fewer bottles sold, but at higher average price).

In 2026, European gin brands will likely emphasize core strengths: for example, London Dry and classic styles reasserting dominance, premium craft offerings with authentic stories, and leveraging Europe’s cocktail capitals to keep gin on menus. We are also seeing some European producers diversify - creating gin-based RTDs and aperitif-like hybrids - to capture casual drinkers (since a hardcore neat gin market is limited). The bottom line for Europe: the boom times have passed, and the region is transitioning into a mature phase where innovation must be balanced with consistency. Brands that evolve with consumer tastes (e.g., focusing on sustainability or authenticity) without alienating their base will find the most success. As Pernod Ricard’s gin marketing head noted, it’s important for brands to “evolve at the same pace as their consumer” - meaning carefully adapt to trends rather than drastically changing identity every year. European gin drinkers in 2026 know what they like, and catering to that informed consumer with quality and credibility will be key.

Asia-Pacific

Asia-Pacific is arguably the new frontier for gin - a region with a smaller historical footprint in gin, but one that’s quickly catching up thanks to globalization of cocktail culture and local craft movements. The Asia-Pacific gin market is diverse, ranging from countries with huge populations just discovering gin, to established economies where gin is a fashionable spirit among the urban middle class. Overall, APAC is expected to be the fastest-growing region for gin from 2024 to 2026 in percentage terms, albeit from a lower base than Europe or North America. Key drivers in Asia-Pacific include rising incomes, a youthful demographic in many countries keen to try new alcoholic beverages, and the localization of gin production using Asian botanicals that appeal to local tastes.

India

One of the most exciting markets in APAC for gin is India. Despite India’s massive population and a long history with the gin-and-tonic (a legacy of British colonial days and quinine tonic water’s use), gin was a relatively small segment in India until recently. That’s changing fast. Premium-and-above gin volumes in India grew by 8% in 2023, and the market is forecasted to sustain about a 5% CAGR from 2023 to 2028.

Several factors are contributing to this Indian gin renaissance. First, local entrepreneurs have launched craft gin brands that resonate with India’s flavors and culture - brands like Greater Than, Hapusa, and Stranger & Sons infuse local botanicals (from cardamom to tea to mango) or draw on Indian spices, creating a product that feels indigenous rather than imported. Indian consumers have responded enthusiastically to these homegrown gins, which often use striking branding and tell a story of Indian heritage. Second, Indian mixology culture is burgeoning: trendy bars in Mumbai, Delhi, Bangalore and beyond are introducing patrons to classic gin cocktails and new creations. As cocktail culture spreads, consumers become more willing to experiment with gin. Third, the aspirational middle class in India is turning towards premium spirits. For a long time, whisky (especially Scotch or Indian-made whisky) dominated India’s spirits market. Now, younger professionals are expanding their palate - gin offers a lighter, more refreshing alternative, especially suited to India’s warm climate and social scenes (think G&Ts at a summer rooftop bar).

The fact that gin can be a showcase for local ingredients is also a plus; as one IWSR analyst noted, gin is an ideal platform for showcasing local botanicals, and India’s rich array of spices and fruits gives distillers plenty to work with. International brands (like Gordon’s, Tanqueray, Beefeater) are present in India too, but it’s the premium and craft category that’s really pushing growth.

Going into 2026, we expect more innovation from Indian gin makers, possibly aged gins or collaborations, and continued strong uptake among urban consumers. The scale of India means even a niche spirits trend can translate to significant volume - global companies are certainly eyeing India as a key growth market for gin. The challenge will be navigating India’s complex liquor regulations (each state has its own taxes and rules) and competing with the enduring popularity of whisky. Nonetheless, the trajectory for gin in India is very positive, making it a crucial market in Asia.

Japan

Japan has emerged as another gin success story in Asia, albeit in a very different way. In Japan, there wasn’t a large indigenous gin culture historically, but the country did have other spirits (like shochu) and a strong cocktail tradition. Over the last few years, Japan has embraced gin, particularly premium gin, to an impressive degree. Premium-plus gin volumes in Japan surged by 31% in 2023, and forecasts predict a remarkable 12% CAGR from 2023 to 2028 in that high-end segment. The gin and tonic is already a well-known drink in Japan (enjoyed in izakayas and bars as a refreshing highball-like cocktail), which has helped drive consumption. Moreover, Japanese producers have thrown their hat in the ring by creating distinctly Japanese gins. Major companies like Suntory introduced products such as Roku Gin, featuring Japanese botanicals (sakura cherry blossom, yuzu peel, green tea, etc.), and smaller distilleries, sometimes coming from a shochu background, began crafting gin using local ingredients. This infusion of local flavor has spurred interest and made gin “cool” in Japan. The country’s legendary attention to craftsmanship also means domestic gins are often of high quality and beautifully packaged, adding to their appeal.

Another interesting dynamic is that Japanese gin became a bit of an export phenomenon - gin enthusiasts globally have sought out Japanese craft gins for their unique profiles, which in turn adds prestige to the category at home. An IWSR director noted that the influx of local players in Japan will keep the category vibrant for years, and indeed we see that happening. Japanese consumers are known to value premium goods, and gin fits well as a premium Western spirit with a Japanese twist. As of 2026, gin in Japan is likely to continue its upward momentum. We anticipate more innovation like barrel-aged gins or limited regional editions within Japan, and increasing integration of gin in high-end cocktails (Japanese bartenders are among the best in the world and often at the forefront of cocktail trends). The only headwinds could be demographic (an aging population that’s drinking less overall) and competition (whisky and sake are strong traditional favorites), but for the younger urban demographic, gin is firmly on the map.

Other Asia-Pacific Markets

Beyond India and Japan, the Asia-Pacific region has several notable gin developments:

- Australia and New Zealand: Australia in particular has experienced a craft gin boom akin to Western countries. Dozens of craft distilleries across Australia - from Four Pillars in Victoria to Archie Rose in Sydney - have gained acclaim. Australian gins frequently leverage native botanicals (such as lemon myrtle, Tasmanian pepperberry, or even unusual ingredients like kangaroo paw flower) to create a unique taste of the “Aussie terroir.” The result is a flourishing domestic gin scene and growing export presence; Four Pillars, for instance, has won international awards. Cocktail culture is vibrant in Australian cities, and gin is a big part of it (e.g., Negroni Week is huge in Melbourne). The growth in Australia’s gin consumption was about 7% back in 2014 and continued strong thereafter. By 2026, Australia’s gin market is maturing but still growing, supported by local love and tourism (visitors often seek out local gins). Neighboring New Zealand also has a handful of boutique gin distillers, and Kiwi gin brands (like Scapegrace) have made a splash internationally.

- China: China remains a relatively small market for gin. Chinese consumers have historically favored baijiu (the local spirit) and more recently whisky and cognac as status spirits. Gin is largely confined to cosmopolitan bar culture in cities like Shanghai, Beijing, and Guangzhou. However, as western cocktail bars proliferate, there is a niche growth for gin, particularly among ex-pats and younger Chinese who travel and acquire global tastes. Some imported gin brands have targeted China, and a few Chinese distilleries are trying gin with Asian botanicals. In 2026, we don’t expect gin to be mainstream in China, but even a niche uptake in a country that large can mean substantial volume growth. The key will be education and positioning gin as a stylish, modern drink (possibly leveraging gin’s low-sugar, natural botanical image for health-conscious urbane consumers).

- Southeast Asia: Various Southeast Asian countries have budding gin scenes. Singapore has become a cocktail capital and a regional hub for craft spirits; it even boasts some local gins (like Tanglin Gin) using regional spices. Bars in Singapore, Kuala Lumpur, Bangkok, and Hong Kong often carry a wide gin selection and do steady business in G&Ts and gin cocktails, especially with the expat community and tourists. The climate (hot, humid) makes gin and tonic an appealing choice. The Philippines, as mentioned earlier, is an outlier in that it’s the world’s largest gin market by volume, but that is almost entirely due to budget local gin consumed as a straight spirit or simple mixed drink by the mass market. Premium gin in the Philippines is a tiny niche by comparison. Thailand, Malaysia, Vietnam, etc., are mostly emerging markets where imported gin is still relatively expensive, but the increasing presence of cocktail bars signals future growth potential, especially as tourism introduces more people to gin drinks.

Overall, Asia-Pacific’s gin outlook for 2026 is one of high growth potential and exciting innovation. The region’s contribution to global gin revenue is set to rise. Many APAC countries have young populations (unlike aging Europe), meaning new legal-age drinkers each year who might pick gin as their spirit of choice. The localization of gin - incorporating local flavors and customs - is playing a major role in adoption. For example, we see gins with botanicals like jasmine, lemongrass, Sichuan pepper, or pandan leaf catering to Asian palates. Moreover, big players are investing: companies like Diageo have introduced smaller brands or limited editions tailored to Asia (e.g., Diageo’s Sichuan Peppercorn Gin in China, or specialty blends for duty-free). The challenge in Asia is navigating varying regulations and alcohol monopolies, and the fact that in some markets, alcohol faces cultural/religious opposition (for instance, majority Muslim countries where alcohol consumption is low). But on balance, Asia-Pacific is where gin brands can really find new growth in 2026, provided they approach each market with cultural intelligence and patience.

With the regional breakdown complete, we can see that gin’s fortunes in 2026 will differ widely by geography. Europe may be in a cooling phase, North America in a slow build, and Asia-Pacific in a strong growth spurt. This creates a complex global picture: gin brands must adopt region-specific strategies, nurturing mature markets with brand loyalty and deeper storytelling, while aggressively pursuing emerging markets with education and tailored products. Next, we’ll examine the broader innovations and trends that are shaping the gin industry, many of which apply across all regions.

Innovations and Emerging Trends in 2026

The gin category has always been characterized by innovation - after all, gin itself was born from infusing neutral spirits with a mix of botanicals, a creative twist that set it apart from other liquors. In recent years, innovation in gin has gone into overdrive, not just in product development (new flavors, styles, and production methods) but also in marketing and how gin is enjoyed. As we head into 2026, several emerging trends are defining the direction of the gin market. These trends respond to current consumer preferences like sustainability and wellness, as well as the need for brands to differentiate in a crowded marketplace. Below, we explore the key innovations and trends to watch, from the contents of the bottle to the ways gin is presented to consumers.

Sustainability and Eco-Friendly Production

One of the most influential trends across the spirits industry, including gin, is a focus on sustainability. Distilleries are increasingly adopting eco-friendly practices in sourcing, production, and packaging - and making it a core part of their brand story. In 2024 and into 2025, many gin producers are touting the use of locally sourced and organic botanicals, reducing carbon footprints, and utilizing sustainable packaging (such as lightweight recycled glass bottles or biodegradable materials). Consumers, especially younger ones, respond positively to brands that demonstrate environmental responsibility. Gin is well-suited to ride this trend: because it’s defined by natural botanicals, there’s an inherent opportunity to talk about agriculture and plant sourcing. For example, distillers might partner with local farms for juniper or herbs, or cultivate botanicals themselves without pesticides.

Innovative projects include gins made from upcycled or waste ingredients - a notable case is the launch of Renais Gin by the Watson family (including actress Emma Watson), which is distilled in part from leftover wine grapes from Burgundy, turning winemaking byproduct into a new spirit. This approach not only reduces waste but creates a unique flavor profile linked to the wine’s terroir. Another brand repurposed the “heads and tails” (the portion of spirit usually discarded during whisky production) to make gin, highlighting a circular economy approach. Additionally, water usage and energy efficiency are in focus; some gin distilleries use renewable energy or recirculated water in cooling processes. Beyond production, sustainable packaging innovations are emerging - like gin packaged in paper-based bottles or refillery pouches to cut down glass usage. All these efforts are becoming major marketing points. In 2026, expect more gin brands to achieve certifications (like B-Corp or carbon-neutral status) and proudly display sustainability credentials, knowing that a significant segment of consumers prefer “planet-friendly” spirits.

Local & Exotic Botanicals (Terroir-Driven Gins)

The botanical flexibility of gin continues to be a playground for innovation. A big trend is emphasizing local or foraged botanicals to create gins that reflect a sense of place (often called terroir in spirits, borrowing the wine term). This trend has seen Japanese gins using native cherry blossoms and yuzu, Australian gins employing things like lemon myrtle or even saline coastal elements (Margot Robbie’s “Papa Salt” gin incorporates coastal succulents and seashell for a briny tang), and African gins using local flora like baobab or bush herbs. By leaning into local ingredients, brands create distinctive flavor profiles and also connect with consumers’ interest in authenticity. In Kenya, for instance, some distillers foray into nearby forests to gather wild juniper berries and other herbs for truly indigenous gin expressions. Europe, too, has examples: Scottish coastal gins with seaweed, Nordic gins with birch sap or lingonberries, etc.

The botanical boldness is not just in using local items but in pushing the boundaries of what flavors gin can encompass. Unusual ingredients like seaweed, cacao nibs, saffron, or even mushrooms have shown up in boutique gin recipes. Importantly, even as exotic botanicals make an appearance, distillers must ensure they maintain juniper as the predominant flavor, per regulations, but there’s a lot of room to layer other notes on top. This trend ties back to sustainability as well - using local means less transport, and often the stories involve supporting local agriculture or conservation (like a distillery planting extra juniper in the wild to ensure future supply). For consumers, these gins offer a novel tasting experience and often an educational element (“try this gin with a botanical you’ve never heard of”). In 2026, expect more hyper-local gin editions, perhaps limited releases that showcase a particular harvest or collaboration with a local botanical garden. This localization also helps smaller distilleries stand out against global brands by offering something unique and rooted in their geography.

Flavor Innovation vs. “Flavored Gin Fatigue”

Flavor innovation was the hallmark of the past decade’s gin boom - with everything from wildly colored “unicorn gin” to fruit-infused pink gins hitting the market. By 2026, this trend has split into two directions. On one hand, flavored and sweet gin variants (like pink berry gins, citrus blends, etc.) remain popular among certain consumer segments and in certain markets. They often serve as entry points for new gin drinkers who might be put off by strong juniper flavor; a strawberry-rosé gin, for example, can entice those who enjoy sweeter profiles. In fact, some reports still count flavored gins as a growth area globally, especially in markets that are newer to gin. Their visually striking appearances (vibrant colors) and crowd-pleasing tastes make them a staple for social media sharing and casual sipping. However, in mature markets, there is clear evidence of flavored gin fatigue - the initial excitement has died down, and sales of these variants are dropping faster than traditional gin. Consumers who were once captivated by novelty flavors have perhaps moved on (some to flavored vodka or hard seltzers, others back to classic gin as they refine their tastes).

Thus, gin makers are recalibrating their flavor innovation. The new focus is on more sophisticated flavor profiles and balanced infusions. Instead of overtly sweet candy-like gins, we’re seeing gins with, say, a hint of orange and cacao, or gin rested with herbs to impart subtle complexity. Essentially, the innovation is moving from high-sugar gimmicks to more craft-oriented tweaks. Additionally, some producers are exploring aged gins - storing gin in barrels (ex-bourbon, wine casks, etc.) to develop vanilla, oak, and spice notes. Barrel-aged gin is an innovative cross-over trend that gives gin a brown spirit character suitable for sipping neat or using in spirit-forward cocktails (subbing for whiskey). It’s niche but growing. In summary, flavor innovation isn’t dead, but it’s maturing: quality over quantity. Gin brands in 2026 will likely be more selective about new flavor releases, perhaps issuing seasonal or limited editions to test interest rather than flooding the shelves continuously. This approach can re-energize consumers’ curiosity without overwhelming them.

Ready-to-Drink (RTD) Gin Cocktails

The convenience trend in beverages has given rise to the booming RTD cocktail market, and gin is at the forefront of this canned cocktail revolution. Consumers increasingly appreciate the ease of cracking open a well-made Gin & Tonic or cocktail without needing mixology skills. In 2025, RTD sales were surging globally (the RTD cocktail market expected to more than double in value from 2023 to 2029), and the momentum carries into 2026. Canned Gin & Tonics and other gin-based RTDs are proliferating, offered by both big brands and craft distillers. Major gin players like Tanqueray, Beefeater, Bombay Sapphire, and Gordon’s each have their branded canned G&T products now, often in various flavors (e.g., grapefruit G&T, elderflower G&T). These products leverage the brand recognition of the gin and promise a bar-quality mixed drink in a portable format. Tanqueray’s canned gin and tonic, for example, has been highlighted as particularly on-trend and successful - delivering true juniper character with balanced bitterness and not overly sweet.

Tanqueray’s ready-to-drink canned Gin & Tonic, exemplifying a major brand’s foray into convenient, on-the-go gin cocktails.

Craft brands are also innovating in RTDs, sometimes going beyond the classic G&T. We see gin spritzes, negronis, brambles, and Collins-style drinks in cans or bottles. Some distillers invent signature canned cocktails tailored to their gin’s profile (for instance, a local distillery might create a canned “Honeydew Collins” highlighting melon notes with their gin). The RTD trend ties into lifestyle shifts: people want premium experiences with minimal effort, be it at picnics, house parties, or just a quick drink after work. Gin, with its light and refreshing image, is well-suited to these contexts.

By 2026, RTD gin cocktails are expected to become even more refined - better quality ingredients (craft tonics, real botanicals in the mix), possibly lower calorie versions to align with health trends, and more variety (e.g., a canned gin basil smash or a negroni sbagliato). The key for brands is ensuring the RTD tastes authentic and not artificial, bridging the gap between a bartender-made drink and a packaged product. For gin marketers, offering RTDs can also be a gateway to bring new consumers into the brand’s universe (someone might try a canned cocktail and then move to buying the full bottle for home). It also allows brands to capitalize on occasions where traditional spirits might not be as convenient. We anticipate continued strong growth in this segment, making RTDs a significant part of gin’s 2026 market strategy.

Low-ABV and Non-Alcoholic “Gin” Alternatives

A major consumer trend impacting all alcohol categories is the rise of the “mindful drinking” movement, which includes interest in low-alcohol and alcohol-free options. Gin is no exception. In 2026, expect to see more low-ABV gins and non-alcoholic gin alternatives on the market. Low-ABV gins are typically distilled gins that are bottled at, say, 20-30% ABV instead of the usual ~40%, offering a lighter option. Non-alcoholic gin alternatives (often called “botanical spirit” or simply alcohol-free spirit) contain 0% alcohol but aim to mimic gin’s flavor by distilling botanicals and extracting essences. This category was essentially created by brands like Seedlip a few years ago, and now many companies (including traditional gin distillers) have their version of alcohol-free gin. The growth numbers are compelling: the low/no alcohol segment is forecast to grow around 7-10% annually in the next few years, outpacing regular alcohol growth. The U.S. and parts of Europe are key markets for these alternatives, driven by Gen Z and Millennials who prioritize health and moderation.

For gin brands, embracing this trend can mean launching a non-alcoholic variant or a line of “gin essences” for mocktails. It’s a way to retain customers who might be taking a break from booze or to offer something at social occasions for non-drinkers. For instance, Gordon’s and Tanqueray have introduced 0.0% alcohol versions of their gin, reproducing the botanical taste without the ethanol. These products often appear in the same gin aisle and leverage the brand name to gain trust. Bartenders are also incorporating low/no gin products in creative low-proof cocktails, further normalizing them. While some purists might argue these aren’t “real gin,” the fact is they compete in the same social usage occasions. By 2026, the line between alcoholic and non-alcoholic offerings under a gin brand portfolio will blur - it won’t be unusual for a gin distillery to promote both a classic gin and a 0% version side by side.

The key for success in this trend is flavor integrity: consumers want the botanical complexity and bite of gin even without alcohol, so constant innovation in extraction techniques (to carry over those flavors) is ongoing. This trend also dovetails with another: lower calorie cocktails - a 0% gin and slim tonic is significantly lower in calories than a standard cocktail, appealing to the fitness-conscious. All said, low/no-alcohol is here to stay, and gin makers in 2026 are taking it seriously as a component of their product mix.

Experiential and Educational Marketing

Innovation in gin is not only what’s in the bottle but also how brands connect with consumers. In a crowded market, providing an experience or deeper engagement can set a gin brand apart. Thus, we see a trend of experiential marketing: distilleries offering immersive tours, gin-making classes, and interactive tastings. By 2025 this was already notable - gin enthusiasts could visit distilleries to blend their own mini-batch of gin or attend cocktail masterclasses that highlight gin’s versatility. These experiences create personal connections and often turn attendees into brand ambassadors.

In 2026, experiential offerings might get more high-tech (perhaps augmented reality distillery tours, or virtual reality cocktail sessions for those who can’t attend in person) as well as more exclusive (e.g., invite-only gin harvest events, or member clubs for early access to special bottlings). Additionally, brands are focusing on education as a marketing tool. Given gin’s nuanced production (do you steep or vapor-infuse botanicals? what is a London Dry vs a distilled gin?), there’s rich content to share. Many brands now produce slick online content or printed guides about gin history, how to taste gin, and cocktail recipes. By educating consumers, they not only demystify gin (helping overcome barriers, especially in places like the U.S. where some find gin confusing) but also reinforce their expertise and credibility.

Digital and AI-Driven Campaigns

Embracing technology in marketing is another emerging trend. A striking example was the “Still G.I.N.” advertising campaign in late 2025, where iconic hip-hop artists Dr. Dre and Snoop Dogg launched a gin brand campaign featuring AI-generated depictions of Frank Sinatra and Sammy Davis Jr. in a stylized 1960s nightclub scene. This campaign fused cultural icons across eras - a clever way to appeal to multiple generations - and it leveraged cutting-edge AI imagery (while taking care to do so ethically with estate permissions). The success of such a campaign provides a playbook for future marketing: blend nostalgia with modern tech to create buzz. Gin brands are likely to explore augmented reality labels (imagine scanning a gin bottle with your phone to see a holographic tour of the distillery) or AI-generated personalized cocktail suggestions for consumers. The message is that innovation isn’t just about new flavors, it’s about new ways to tell your story. The “Still G.I.N.” ad also underlined an important marketing insight: focus on narrative and lifestyle, not just product specs.

In a world where consumers have countless gin choices, an emotional or story-driven appeal can make a brand memorable. We anticipate more collaborations between gin brands and artists, musicians, or even fashion designers to position gin in lifestyle contexts (some premium gins have already sponsored music festivals or art events to align with a creative, upscale lifestyle).

Cocktail Culture and Mixology Trends

Finally, one cannot talk about gin trends without touching on cocktails. Gin remains one of the cocktail world’s foundational spirits, and trends in mixology often drive gin consumption. As of 2026, cocktail innovation is thriving, and gin is benefiting from that. Bartenders are using advanced techniques - fat-washing, clarification, fermentation - to create novel gin cocktails that get press coverage and social media buzz. For instance, a mixologist might clarify a classic milk punch with gin or create a foaming gin sour with aquafaba and rare ingredients. These cutting-edge creations keep gin relevant for cocktail aficionados always seeking something new. Meanwhile, classic gin cocktails are enjoying enduring popularity: the Negroni has become a globally beloved drink (even spawning a spinoff trend with the “Negroni Sbagliato” going viral), and the dry Martini is perennially chic, with endless debate about gin brands and ratios. Gin’s mixability means it’s often at the center of cocktail trend pieces - such as “top trending cocktails of 2025” lists which inevitably feature multiple gin drinks.

Additionally, food pairing with gin is an emerging concept. High-end restaurants and bars have started doing gin pairing menus, suggesting certain gins (or gin cocktails) with specific dishes, akin to wine pairings. This elevates gin’s status in the culinary world and opens up new consumption occasions (a specific gin to go with oysters, for example). By 2026, we might even see dedicated gin-and-food tasting events or books on the subject. All these cocktail-centric trends reinforce one thing: gin’s versatility is its superpower. As long as mixologists continue to find inspiration in gin, it will maintain a vital place in bars globally. For brands, supporting the cocktail community (through sponsorships, competitions like “best gin cocktail” contests, etc.) is a wise move to stay at the heart of this innovation.

In summary, the innovations and emerging trends shaping the gin market in 2026 cover a broad spectrum - from product innovation (sustainable, local, low-alcohol) to marketing innovation (experiences, digital campaigns) to consumption innovation (RTDs, new cocktail serves). Gin is evolving to meet the contemporary consumer where they are: caring about health and planet, craving convenience yet also willing to savor quality, and always looking for a story or experience to share. Brands that stay ahead of these trends - or better yet, set them - will strengthen their relevance and appeal. The next section will build on these insights to discuss concrete strategies gin brands can adopt for success in 2026’s competitive landscape.

Strategies for Brand Success in 2026

Facing a rapidly changing market, gin brand owners and marketers in 2026 need a clear game plan to thrive. The days when a simple “London Dry” label and a quirky story guaranteed success are over; today’s environment demands both consistency with brand heritage and bold adaptation to new trends. Based on industry best practices, expert opinions, and the trends outlined above, here are key strategies for gin brands aiming to achieve sustainable growth and strong consumer connections in 2026:

Embrace Authenticity and Build Trust

In a crowded marketplace, authenticity is one of the most valuable currencies a brand can have. Consumers have become savvy - they can sense when a brand is just riding a fad versus when it has genuine passion and expertise in its craft. For gin brands, this means doubling down on what truly makes your product special and communicating that transparently. Share the story of “who” is behind the gin and “how” it’s made in an open, engaging way. For instance, highlight the master distiller’s experience, the history of the distillery, or the local community it’s tied to. Provide clear information about your botanicals and production process - if it’s a small-batch copper pot distillation with handpicked herbs, let people know. Such details demonstrate expertise and love for the product, which in turn makes consumers want to trust and try it.

According to industry observers, consumers these days “want to know how and where their gin is made, and whether the brand aligns with their values”. This alignment could be about sustainability, local sourcing, or social responsibility. A practical step is to ensure your gin carries a byline or story on its packaging and website - essentially an “About us” that isn’t just marketing fluff but gives real insight into the brand’s ethos. An authentic narrative invites people into the world of the brand, making them feel part of something more than just a transaction. Trust also comes from quality consistency - maintain high standards so that each bottle delivers the flavor and smoothness you promise. If you earn a reputation for reliability and sincerity, your brand will more likely be bookmarked in consumers’ minds and recommended among friends.

Align with Premiumization - but Deliver Value

Premiumization has been a key driver of gin market growth, but succeeding in the premium segment is not just about charging a high price - you must justify the premium in consumers’ eyes. Brands should focus on what sets them apart from competitors and communicate those differentiators clearly. Is it an exotic botanical blend that no one else has? A unique geographical indication (e.g., “Isle of Harris gin - infused with local sea kelp”)?

An extra-smooth base spirit distilled from grapes instead of grain? Identify the factors that elevate your gin and weave them into your branding and messaging. Also, consider tangible signals of quality: upscale packaging (heavy glass bottle, elegant label), awards and accolades from spirits competitions (a gold medal from IWSC or San Francisco Spirits Competition can be a selling point), and associations with exclusive experiences (being the “official gin” of a high-end event or hotel bar).

In 2026, with economic uncertainties, consumers may scrutinize luxury purchases more; thus, ensure that when someone splurges on your gin, they feel the worth in the experience - be it superior taste or brand prestige. At the same time, remain mindful of pricing strategy. Premium doesn’t mean pricing out of all reach; often, consumers will pay a bit extra for a clearly better product, but if prices soar too high without obvious reason, they may opt for a competitor. A tactic some brands use is offering different tiers: a classic gin at a mid-premium price and a limited-edition ultra-premium release at a high price for enthusiasts. This covers both ends and allows the core product to remain accessible enough to build a broad following, while still capturing the top-end market with special offerings.

Harness Storytelling and Lifestyle Marketing

Gin is not just a liquid, it’s a lifestyle - at least that’s how successful marketing frames it. Effective storytelling can transport consumers into the world your brand creates. Whether that world is the glamour of the 1920s jazz age, the wild ruggedness of a coastal distillery, or the cutting-edge urban cocktail scene, pick a narrative and amplify it. The example of the Still G.I.N. campaign is instructive: it didn’t talk about ABV or juniper; it painted a picture of a cool nightclub with cultural icons, selling an aspirational vibe. Similarly, your brand might emphasize being the gin of carefree summer nights under the stars, or the gin of connoisseurs who appreciate fine craftsmanship. Use social media, content marketing, and partnerships to tell these stories. Perhaps publish a short video series featuring the people and inspirations behind your gin. Collaborate with lifestyle influencers - not just spirits influencers, but perhaps a travel blogger who brings your gin on a journey, or a chef who crafts dishes to pair with it. The idea is to get people to feel something about your gin, beyond just “it tastes good.” When you achieve that emotional connection, your brand becomes shareable and recommendable.

Additionally, consider aligning with causes or communities that reflect your brand values, which can deepen the narrative. For instance, if your gin is all about mountain botanicals, perhaps sponsor environmental initiatives in the mountains or events like hiking meetups - this reinforces the identity you’ve cultivated and shows you walk the talk. By showcasing the real experiences and expertise behind your brand story, you prove you’re not just churning content for SEO but genuinely engaging people, which ultimately helps organic reputation.

Innovate Carefully and Purposefully

Innovation remains critical - no brand can afford to stagnate - but as discussed earlier, it should be purposeful innovation that aligns with your brand and consumer needs, not gimmicks. In a declining or slow market (like gin in the UK or US), there’s pressure to throw new ideas out to spur sales. However, too much rapid-fire innovation can dilute your brand identity and confuse consumers. Instead, adopt a strategy of measured innovation. This might mean releasing one well-researched new variant per year (for example, a limited edition that has a story, like “harvest 2026 special edition with locally foraged truffles”), rather than multiple random flavor extensions. Before innovating, use market research and feedback to gauge what consumers really want. Are they asking for a sloe gin or a navy strength version of your product? Are they interested in a canned cocktail from your brand? Align innovation with those insights.

Diageo’s innovation director noted the importance of being willing to “celebrate the kills” - acknowledging when an innovation fails and learning from it. In practical terms, set up a process to pilot new ideas (maybe small batch releases or limited regional launches) and track performance. If something doesn’t click, it’s okay to sunset it and redirect focus. This approach keeps the brand agile but not reckless. Also, some innovations could be in format or route-to-market rather than product alone: for example, a gin subscription service delivering seasonal infusions to loyal customers, or leveraging tech by having a chatbot sommelier that helps users pick cocktails. These kind of service or experience innovations add value without necessarily changing the core liquid.

Leverage Cocktail Culture & On-Premise Influence

For any spirit, winning the on-premise (bars, restaurants) battle is key to winning the war. Ensure your brand is visible and favored in cocktail bars, as on-premise trends often influence off-premise sales. Strategies include building strong relationships with bartenders and mixologists. This could mean having a dedicated brand ambassador who visits bars to do tastings with staff and provide training on making great gin cocktails. Often, if bartenders like a gin and know its story, they’ll recommend it to patrons or include it in signature drinks.

In 2026, with gin’s growth highly tied to cocktails, make sure you’re providing bars with what they need - be it support materials, coasters, visibility in menus, or even custom cocktail recipes developed for that bar. One recommendation from industry analysis was to “stay visible in on-premise” and use the window when, say, other imported brands might be struggling (like during tariff increases) to step in. The idea is to secure that menu real estate. Perhaps sponsor a cocktail-of-the-month at a popular venue that prominently features your gin. Meanwhile, don’t neglect home cocktail makers: provide easily accessible recipes on your website or social channels, host virtual cocktail classes, and partner with cocktail influencers or kit providers (imagine a home Negroni kit that includes a bottle of your gin). The easier you make it for consumers to enjoy your gin in a great cocktail, the more likely they are to keep buying it. Keep an eye on cocktail trends and ensure your brand stays relevant to them. For instance, if espresso martinis are trending, perhaps promote a recipe for a “Red Snapper” (gin Bloody Mary) at brunch as an alternative - positioning gin in contexts where vodka typically plays, to encourage switches.

Strengthen Distribution and Market Presence

Even the best gin will falter if it’s not available where consumers are shopping. A key strategy is to bolster your distribution networks and adapt to any logistical challenges. If you’re an international brand facing distribution hiccups (like those caused by the aforementioned tariffs or by post-pandemic shipping issues), consider strategies such as partnering with local bottlers or distributors to reduce friction. In some cases, local production under license might even be viable if tariffs are prohibitive - producing your gin in the target market to avoid import duties (as some whiskey and beer companies do). For craft brands, focus on building relationships with a few key distributors who are enthusiastic about your product rather than spreading thin. Another aspect is omnichannel presence: ensure that your gin is not only in brick-and-mortar stores but also in online retail channels. The rising influence of online retailing for spirits is a notable trend - many consumers now discover and purchase alcohol through apps and websites. Work with popular alcohol delivery services or online marketplaces to feature your brand (possibly offering bundled deals or holiday gift packs exclusive to online shoppers).

Additionally, as pandemic times showed, direct-to-consumer (DTC) shipping (where legal) can be a lifeline - if your jurisdiction allows it, invest in a good e-commerce platform on your own site. With DTC, you can also gather valuable consumer data for remarketing. In markets like the U.S. where DTC spirits shipping is limited but evolving, stay abreast of legal changes; being an early mover in DTC could give you an edge in consumer loyalty. Don’t ignore international expansion either: if Europe is saturated, perhaps the next growth step is entering an Asian market with a local partner. Identify 1-2 emerging markets that fit your brand (e.g., a craft gin with exotic botanicals might do well in high-end bars in Singapore or Dubai) and formulate an entry strategy (maybe via duty-free channels first to test the waters).

Engage in Cross-Category Collaboration and Partnerships

To stand out, sometimes you should not go it alone. Cross-industry collaborations can expose your gin to new audiences. We’ve seen gin brands partner with fashion labels for limited-edition bottle designs, or with music artists for co-branded promotions (like the Ryan Reynolds and Aviation Gin case - a celebrity affiliation that massively raised that brand’s profile). Another approach is collaborating with other drink categories. For instance, partner with a tea brand to create a gin-and-tea infusion kit (appealing to those who love tea and might be intrigued by gin’s botanicals). Or collaborate with a craft brewery to do a beer-gin combo release (like aging gin in barrels that held an IPA, and vice versa, then marketing the pair). These kinds of crossovers generate buzz and can yield interesting products that garner media coverage. They also underscore that your brand is culturally savvy and not stuck in a silo. When planning partnerships, ensure they feel natural - something your core fans would also appreciate, not a completely out-of-left-field stunt.

Additionally, multiple retail partnerships can be valuable for consumer trust. Be in upscale liquor boutiques and accessible grocery chains if possible, to capture different buyers. If recommending places to buy on your site or socials, list a few (e.g., “available at Waitrose, Total Wine, and Drizly”), which both aids the consumer and shows broad availability.

Monitor and Adapt to Consumer Feedback

Brands that listen win. In 2026, leverage the fact that feedback is everywhere - from social media comments, reviews on sites, to focus group studies - to constantly refine your strategy. If aficionados are saying your latest batch’s flavor is slightly off, investigate and address it before it becomes a larger reputation issue. If people keep requesting a type of gin (like “when will you make an Old Tom style?”), perhaps it’s worth considering in your pipeline. Use analytics tools to see what content or product on your site gets the most attention - it might guide where the interest lies. Importantly, engage in two-way communication: respond to consumer inquiries with substance (not just a canned line). If someone tweets at the brand complaining their bottle’s cork was broken, publicly apologize and offer a fix; this turns a negative into a demonstration of customer care. Also, encourage user-generated content - for instance, a hashtag for cocktails made with your gin - and then reshare the best ones (with credit). This not only provides you with free content, but also builds a community feel. A satisfied, engaged community around your brand can become your best marketing asset.

Diversify Portfolio Thoughtfully (Without Overextending)

Many gin producers don’t just sell one gin; they have a range - perhaps a classic dry, a citrus gin, a navy strength, a slow gin, etc. A diverse portfolio can capture different market segments (e.g., a lower-ABV pink gin for casual drinkers, a high-proof gin for mixologists). However, each addition should have a rationale. By 2026, consider having coverage for key segments: a) your flagship gin (the hero product), b) maybe a flavored or contemporary style gin (to cater to those who like a twist), c) a premium upgrade (barrel-aged or limited edition for collectors), and d) a low/no alcohol variant (to not miss out on that segment). Ensure each product has its own identity but still under the umbrella of your brand values. Avoid launching so many versions that they cannibalize each other or confuse shelf space. Every product should earn its keep. Also, if your brand equity is strong, you might extend into related categories carefully - for example, some gin brands release a vodka or an aperitivo liqueur under the same brand. This can work if your brand stands for botanical expertise, for instance (maybe you create an amaro). But be cautious: core fans might see it as dilution if not executed well.

Focus on People-First Content and Community Building

Lastly, a strategy that aligns with both marketing and public relations is to create content that genuinely benefits and engages your audience, rather than just pushing for sales. Gin brands can do this by, say, maintaining a blog or video series with educational and entertaining content: e.g., “Cocktail 101: Easy Gin Drinks for Beginners,” “The History of Gin in 5 Cocktails,” or interviews with bartenders or herbalists. By providing value beyond the product, you position your brand as a thought leader and reliable source in the spirits space. This content can improve your search rankings (as it’s likely to be rich and keyword-relevant organically) and also give media a reason to mention you (they might reference your gin guide in an article about spirits).

Additionally, support the community of gin enthusiasts. Perhaps host contests (like a home bartender competition making drinks with your gin) or create a loyalty club where members get exclusive content or early access. Make your consumers feel heard and rewarded. Some brands have had success with crowdfunding special editions, effectively turning loyal customers into investors/stakeholders with a deeper bond to the brand. People-first also means if there is any issue (say a batch recall or a controversial ad), handle it transparently and with the customer’s perspective in mind, not just corporate defensiveness.

To summarize the strategic playbook: know your brand’s core and broadcast it (Who you are, Why you do it); ensure everything from product to promotion aligns with delivering a great, authentic gin experience; innovate where it counts, and engage the people who support you at every step. 2026’s gin market won’t be the free-for-all of a decade ago; it will reward brands that are highly competent, credible, and connected with their audience. By following these strategies - focusing on quality, storytelling, smart innovation, and genuine engagement - gin brands can navigate the year’s challenges and capture its opportunities, setting themselves up for long-term success even as fads come and go.

Addressing Challenges in 2026

Even with the best strategies and strongest trends in one’s favor, the gin industry in 2026 must confront a set of challenges head-on. These challenges range from external market forces to category-specific issues that, if left unaddressed, could hinder growth or erode brand standing. Below we identify the key challenges and discuss how stakeholders can address them to mitigate risks:

Challenge 1

Market Saturation and Category Fatigue - In traditional markets especially, an overabundance of gin brands and expressions has led to consumer fatigue and a contraction in sales. When faced with a wall of dozens of similar-looking gin bottles, consumers can become overwhelmed or indifferent. Addressing this requires differentiation and rationalization. Brands should evaluate their product lines and focus on hero products rather than trying to occupy every niche. It may be better to have a tighter portfolio that sells consistently than a sprawling range where some expressions languish. If you’re a retailer or distributor, curate your gin selection to highlight diverse, high-quality options rather than every possible SKU; this can actually boost overall category sales by not diluting consumer attention. For brands, sharpen your positioning - make it immediately clear what sets your gin apart (be it flavor profile, heritage, or production method) so a shopper or bar manager has a compelling reason to choose it over others.

Additionally, ramp up consumer education and engagement to combat fatigue. Sometimes people retreat from a category when they feel they don’t understand it anymore. By providing clarity (through tastings, flavor charts, or simplified messaging like “this gin = classic juniper, that gin = floral and light”), you can re-energize interest. Essentially, fight saturation by being distinctly you and helping the consumer navigate the choices. Over time, we may see some natural consolidation in the industry (not every small gin brand will survive a downturn), so those who stand for something memorable and maintain quality will outlast the shakeout.

Challenge 2

Competition from Other Spirits and Beverages - Gin isn’t competing in a vacuum; consumers have many options from whiskey to vodka to tequila, not to mention the explosion of ready-to-drink beverages and even non-alcoholic substitutes. Lately, agave spirits (tequila, mezcal) have been stealing the limelight that gin once had. To ensure gin isn’t left behind, brands and the industry as a whole must continually reassert gin’s relevance and versatility. One approach is through cocktail culture: gin has a unique botanical character that no other spirit can replicate, which shines in certain cocktails (a Negroni with tequila or vodka just wouldn’t be a Negroni). Emphasize these classic uses and invent new ones; for instance, push the narrative that gin can be a year-round spirit (not just a summer G&T) by promoting warm gin cocktails or gin in festive punches for winter holidays.Also, highlight flavor advantages: a consumer who loves spiced or citrusy flavor might be swayed that gin offers those naturally through its botanicals, vs. the vanilla/caramel notes of whiskey or the neutrality of vodka. Innovation can play a part - for example, developing barrel-rested gins that appeal to whiskey drinkers bridging categories, or creating gins with exotic flavor twists that intrigue a market bored of sweet flavored whiskeys.