.svg)

.png)

.gif)

Introduction

This report was developed by OhBEV, an alcohol marketing agency working at the intersection of brand, data, and culture across wine, spirits, beer, and emerging beverage categories. We created this outlook to move beyond surface-level “trend lists” and provide decision-makers with a clear, experience-driven view of what is actually reshaping the U.S. wine market - from consumer behavior and pricing power to distribution dynamics, regulation, and climate risk.

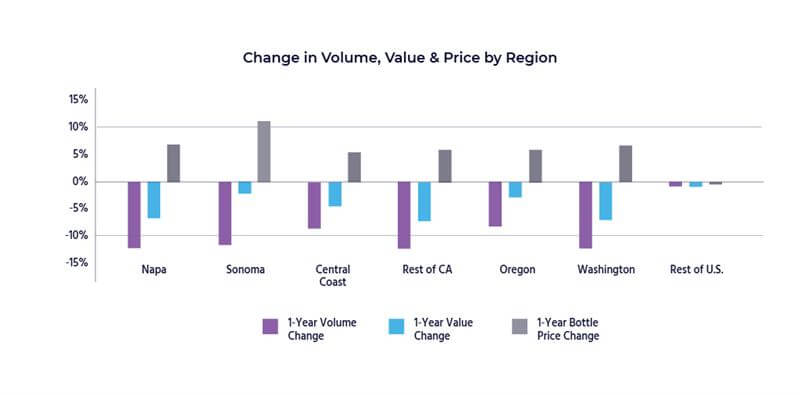

The U.S. wine industry enters 2026 at a crossroads. The past year (2025) proved to be an inflection point marked by converging challenges: a stubborn oversupply of wine (especially at the low end), sluggish demand among younger consumers, and abrupt tariff shocks that upended import pricing. Despite early hopes of post-pandemic recovery, 2025 brought a sobering reality check. Consumption volumes continued to slip (U.S. wine sales by volume were roughly flat to slightly down, extending the prior declines), and wineries large and small were forced to adapt to a rapidly evolving market landscape.

Key hurdles from 2025 included an ongoing “demand reset” - younger generations drinking less wine than their predecessors - and a persistent glut of bulk wine and grapes that pressured prices. Many producers ended 2025 still grappling with excess inventory, elevated storage costs, and an uncertain economic climate. On top of that, a wave of neo-prohibitionist health messaging gained traction, as consumers increasingly questioned alcohol’s role in their wellness. In short, much of the industry spent the year in recalibration mode, rethinking product portfolios, marketing approaches, and distribution strategies to align with these new realities.

Yet 2025 also sowed the seeds for a potential turnaround. The resolution (at least partially) of a transatlantic trade dispute removed the threat of extreme import tariffs, and there are early signs that the worst of the oversupply might be easing. Many in the trade view 2026 as a year of cautious optimism - a chance to stabilize and even return to modest growth, provided that companies innovate and respond to the trends at hand. Millennials and Gen Z consumers, long considered wildcards for wine, are gradually gaining purchasing power and could still be won over with the right tactics (think authentic stories, convenient formats, and health-conscious options). Meanwhile, direct-to-consumer channels and on-premise venues are finding creative ways to re-engage customers, and sustainability efforts are becoming central to brand value propositions.

If 2025 was about confronting hard truths, 2026 is about adaptation and opportunity. The year ahead offers a chance for the U.S. wine sector to turn the page on a difficult chapter and implement forward-looking strategies. From recalibrating pricing tiers and embracing no/low-alcohol offerings, to doubling down on digital engagement and negotiating a new trade landscape, this year will test which businesses can innovate versus those stuck in old paradigms. Importantly, the geopolitical and economic environment remains in flux - meaning wine businesses must be more agile than ever.

In this outlook, we’ll explore the major forces shaping the U.S. wine market in 2026, drawing on the latest data and industry insights. Each section delves into a critical aspect of the market, from tariff and trade developments to shifting consumer dynamics, premiumization trends, category innovations, and beyond. We’ll also highlight strategic recommendations for wine marketers, distributors, investors, and brand owners looking to navigate the year ahead. By understanding the lessons of 2025 and the emerging trends of 2026, stakeholders can position themselves to not just survive, but thrive in a rapidly changing wine landscape.

Tariff and Trade Developments Shaping 2026

Trade policy was the single most disruptive external force to hit the U.S. wine market in 2025, and its effects continue to shape competitive dynamics entering 2026. The turning point came in April 2025, when President Donald Trump announced the sweeping “Liberation Day” executive order on trade. The policy imposed a baseline 10% import tariff on virtually all imported goods and introduced additional country-specific duties slated to take effect by mid-year.

For wine, the implications were immediate and severe. The European Union - accounting for roughly 72% of U.S. wine imports by value - was targeted with an additional 20% punitive tariff tied to trade imbalances. Combined with the baseline levy, EU wines were suddenly facing a 30% total import duty. Importers prepared for dramatic cost increases, halted shipments, and explored re-routing strategies to avoid the full impact. Consumers, meanwhile, faced the prospect of 25-30% retail price increases on many Old World wines.

The Mid-2025 Trade Truce

The most extreme scenario was narrowly avoided. On July 27, 2025 - days before the full 30% tariff was due to take effect - the U.S. and EU announced a framework trade deal. Implemented on August 1, the agreement replaced the layered tariff structure with a flat 15% U.S. import duty on nearly all EU goods, including wine. French, Italian, Spanish, and other EU wines entered late 2025 facing a 15% tariff - roughly half the initially threatened rate.

Both sides also signaled a shared objective of eliminating beverage alcohol tariffs altogether. A “zero-for-zero” arrangement for wine and spirits remains under active negotiation. As of early 2026, however, wine continues to carry a 15% U.S. import tariff pending a final resolution.

For the U.S. wine market, this compromise significantly reset expectations. While still meaningful, a 15% tariff prevented the severe dislocations that a 30% duty would likely have caused across pricing, availability, and demand.

Pricing Impact on Imported Wines

Even at 15%, tariffs function as a direct tax on imported wine, and most of that cost has flowed through the system. Under the original plan, a $15 wholesale Italian wine would have incurred $4.50 in tariffs, raising its landed cost to $19.50 and pushing retail pricing to roughly $31 - about 29% above its pre-tariff price of ~$24. Under the 15% compromise, the same wine absorbs a $2.25 tariff, lands at $17.25, and typically retails near $29 - still around 20% higher than before tariffs.

The difference of several dollars per bottle proved critical in preserving demand, particularly in the $15 - $30 segment. High-end imports were also affected. A $50 Champagne that previously retailed near $80 now often lands in the mid-$90s, rather than exceeding $100 under a 30% scenario.

Overall, European wines on U.S. shelves are commonly 15-25% more expensive than a year earlier. Importers have passed through most of the added costs, though many absorbed a portion - especially on high-volume SKUs - to remain competitive.

Supply Chain Whiplash

The tariff rollout created significant supply chain volatility throughout 2025. In the spring, uncertainty surrounding the impending 30% duty led many importers to pause EU shipments entirely. By early summer, inventories of popular wines thinned just as seasonal demand for categories like Provence rosé and Italian Pinot Grigio peaked.

Once the 15% rate was finalized, importers rushed to restart orders. This sudden reversal created a classic “bullwhip” effect: freight bottlenecks, administrative delays, and higher logistics costs. Industry estimates suggested roughly $1 per bottle in additional shipping and compliance expenses during autumn 2025 as companies scrambled to restock.

By late 2025, most logistical disruptions had eased, but import inventories entering 2026 are notably leaner. Importers are managing stock conservatively, favoring just-in-time ordering to limit capital exposure - even at the risk of periodic outages on niche wines.

Competitive Dynamics: Imports vs. Domestic Wines

A central question has been whether higher import prices would materially shift demand toward U.S. wines. In theory, tariffs should advantage domestic producers by narrowing price gaps. There was early evidence of this effect in 2025: a $20 California Pinot Noir appeared more attractive alongside a French Côtes du Rhône that jumped from ~$24 to $29.

Some retailers reported modest lifts in U.S. wine sales in late Q2 and Q3 2025 as European prices adjusted. However, the overall impact has been limited. According to Winescape, domestic wines had not captured significant import share by Q4 2025 despite the tariffs.

Several factors explain the muted response. Many distributors and retailers stockpiled European wines ahead of the tariff deadline, delaying full price pass-through. Consumer preferences - especially for heritage regions - proved sticky; a Barolo loyalist did not easily substitute with California Cabernet. Finally, U.S. producers faced rising costs of their own, limiting aggressive pricing moves.

That said, 2026 may show a stronger shift as pre-tariff inventory clears and all new shipments reflect the higher cost base. Domestic wineries are expected to continue emphasizing their “tariff-free” positioning, while price-sensitive consumers increasingly explore U.S., South American, and Australian alternatives. The playing field in the $15-$30 range has tilted slightly toward domestic brands, though capitalizing on that tilt requires marketing and distribution execution - not price alone.

Hidden Costs for U.S. Producers

Tariffs did not deliver a clean competitive win for American wineries. The globalized nature of wine production means many critical inputs are imported. An estimated 70% of U.S. wine bottles are sourced from abroad, primarily China, France, and Mexico. Under the 2025 measures, Chinese glass faced tariffs near 20%, while European glass carried 15%.

As a result, packaging costs rose sharply. Industry estimates suggest California wineries saw bottle costs increase by $0.50-$1.00 per bottle. Closures, capsules, and equipment - often sourced from Europe - also became more expensive. These increases compressed margins and forced domestic producers to raise prices modestly, narrowing their advantage over imports.

In practice, a Napa Cabernet did not suddenly become inexpensive relative to Bordeaux, because the Napa winery itself was paying materially more for glass, corks, and other components. In response, many wineries are seeking alternative suppliers, renegotiating contracts, or accelerating adoption of lighter or alternative packaging formats such as cans and PET bottles.

Legal and Trade Uncertainty Entering 2026

As 2026 begins, the tariff regime remains unresolved. Negotiations continue toward a potential tariff-free outcome for wine and spirits, which would significantly ease pressure on importers and could stabilize prices - though not necessarily return them fully to pre-tariff levels given other cost increases.

At the same time, legal uncertainty looms. A coalition of wine importers and hospitality businesses has challenged the “Liberation Day” tariffs in court, arguing executive overreach. The case moved quickly through lower courts in late 2025 and is widely expected to reach the U.S. Supreme Court in 2026. A ruling against the tariffs could abruptly end or materially alter the policy, reshaping pricing overnight.

Conversely, failed negotiations or adverse rulings could entrench the 15% tariff - or even escalate tensions. Importers are hedging by diversifying sourcing toward tariff-light countries, while domestic producers are cautious about assuming the competitive gap will widen further.

Export Headwinds and Retaliation Risks

The tariff conflict has also weighed heavily on U.S. wine exports. Although the EU refrained from retaliation in 2025 - despite earlier threats of a 50% duty on American whiskey - exports still declined. A strong dollar made U.S. wines less competitive abroad, and political fallout with Canada proved especially damaging.

In mid-2025, most Canadian provinces (excluding Alberta and Saskatchewan) imposed bans on U.S. wine and spirits in protest of U.S. trade actions. As a result, U.S. wine exports to Canada collapsed, falling more than 90% year-on-year in Q3 2025. As of January 2026, most restrictions remain in place.

Overall, U.S. wine export value declined sharply in 2025 and is not expected to rebound quickly. Export-oriented wineries are redirecting efforts toward Asia-Pacific markets such as Japan, South Korea, and Singapore, where trade terms are more favorable, and exploring DTC-enabled international channels where legal.

Outlook

Trade and tariffs remain a defining variable for the U.S. wine market in 2026. The turbulence of 2025 has settled into a more predictable - but still elevated - 15% duty on European wines. Whether this becomes a long-term reality or a temporary disruption depends on diplomacy and the courts.

In the meantime, importers are rebalancing portfolios toward tariff-light origins, domestic brands are leaning into “buy American” messaging, and exporters are diversifying markets. The lesson of 2025 is clear: trade policy can shift rapidly, and flexibility is no longer optional. Wine businesses that manage costs tightly, communicate clearly with customers, and maintain sourcing optionality will be best positioned to navigate whatever comes next.

Wine Market Overview 2026

After years of disruption, the U.S. wine market enters 2026 in a phase best described as stabilization rather than recovery. The steep volume declines that defined the period from 2019 through 2024 are slowing, and industry analysts broadly agree the market is approaching a bottom. However, any return to growth will be modest, uneven, and driven primarily by price and mix rather than a resurgence in consumption.

In short, 2026 is shaping up as a year of consolidation: fewer bottles sold, higher average prices, and continued pressure on cost structures.

Volume and Value Projections

Most industry forecasts converge on the same conclusion: U.S. wine volume in 2026 will be roughly flat. Following consecutive annual declines of approximately - 1% to - 5% between 2019 and 2024, preliminary estimates suggest 2025 ended around flat to - 1% in total volume, according to data from bw166 and Gomberg Fredrikson. That easing of decline marks a meaningful inflection point.

Looking ahead, projections for 2026 range from a modest - 0.5% decline to a +0.5% increase in volume. In practical terms, this means total wine sales are expected to hover very close to 2025 levels. The consensus leans slightly negative, reflecting structural headwinds in demand, but even flat performance would represent a psychological win for an industry that had feared continued erosion.

On the value side, the outlook is more constructive. Dollar sales are projected to rise by approximately +2% to +4% in 2026, building on estimated +1% to +2% growth in 2025. This growth is driven almost entirely by premiumization and price increases rather than higher consumption. Wineries implemented broad price adjustments in late 2024 and throughout 2025 to offset inflation in labor, glass, logistics, and energy. Those increases will be fully reflected across 2026.

Silicon Valley Bank’s State of the U.S. Wine Industry report reinforces this dynamic. While wines priced below $10 continue to decline sharply, segments above $15 are holding steady or growing, lifting the overall average bottle price even in a flat-volume environment. The result is a “less, but better” market: fewer cases sold, but higher revenue per case.

Growing Polarization by Price Tier

The divergence between price segments continues to widen. Ultra-premium and luxury wines - generally $50 and above - remain resilient. Demand in this tier is relatively inelastic, supported by affluent consumers and collectors who maintained purchasing through 2025. Volumes here were flat to slightly positive last year and are expected to remain stable in 2026.

The $15-$49.99 segment, often described as premium or “masstige,” continues to perform best in aggregate. These wines posted year-on-year gains in 2025 and are projected to deliver low-single-digit volume growth in 2026. This tier benefits from two converging forces: Baby Boomers trading up while drinking less, and Millennials prioritizing quality over quantity.

At the opposite end, the sub-$9.50 segment remains under severe pressure. After multiple years of double-digit volume declines, this tier continues to contract and is expected to do so again in 2026, albeit potentially at a slower pace as weaker players exit. Supermarket jug wine and generic box wine have been hit hardest. By the end of 2026, wines priced under $10 will represent a significantly smaller share of the total market than they did just a few years ago. This polarization explains why value growth persists even as total volume stagnates.

Macroeconomic Forces Shaping Wine Demand

Economic conditions in 2026 remain mixed and continue to shape purchasing behavior across channels.

Interest rates, raised aggressively between 2022 and 2024, plateaued in 2025 but remain at their highest levels in decades. For wine businesses, this has direct consequences. Distributors and retailers face higher financing costs to carry inventory, reinforcing the conservative ordering patterns seen throughout 2025. Wineries with debt - particularly those that expanded capacity or acquired vineyards during the low-rate era - are experiencing higher interest expenses, squeezing margins and marketing budgets.

Inflation, while no longer surging, remains elevated. After peaking in 2022, U.S. inflation cooled to roughly 3% by late 2025, with a brief uptick to around 3% year-on-year in Q3. Forecasts for 2026 place inflation in the 2.5-3.5% range - well below crisis levels, but still above the Federal Reserve’s long-term target. Importantly, many wine input costs have reset at structurally higher levels. Glass, freight, energy, insurance, oak, and labor are unlikely to return to pre-pandemic pricing even if inflation moderates further.

For consumers, this environment translates into constrained discretionary spending. Rising costs in housing, groceries, fuel, and insurance limit flexibility in beverage budgets. As a result, mainstream wine buyers remain price-sensitive and promotion-driven, opting for known brands or lower-priced weekday options while reserving premium purchases for specific occasions.

Growth, Employment, and Consumer Confidence

U.S. economic growth remains sluggish but positive. After a contraction in Q1 2025 - linked in part to tariff disruptions and a brief government shutdown - the economy rebounded in Q2 and returned to modest growth by Q3. Forecasts for 2026 call for GDP growth of approximately 1-2%, avoiding recession but offering little momentum.

.png)

Unemployment rose to around 4.5% in late 2025, the highest level in four years, and could edge higher in early 2026. While still historically low, any softening in the labor market weighs on consumer confidence. Indeed, sentiment indexes at the end of 2025 were near record lows, comparable to the pessimism seen in 2022. Political uncertainty, cost-of-living pressures, and macro instability have left consumers cautious.

This caution is unevenly distributed. Higher-income households benefited from equity market strength in 2025, preserving spending power at the top end. These consumers remain critical to premium wine performance and are expected to continue buying in 2026, albeit selectively. The result is a bifurcated market: affluent consumers sustain premium demand, while the middle market remains defensive.

Inventory and the Oversupply Reset

Oversupply has been one of the most persistent drags on the U.S. wine market. By the end of 2024, tanks and warehouses - particularly in California - were burdened with excess wine from large vintages earlier in the decade. The hope entering 2025 was that supply discipline would finally rebalance the system.

That correction is now underway, though at significant cost to growers. California’s 2025 grape harvest was among the smallest in decades. Early estimates place the crush below 2.5 million tons - potentially the lowest since the late 1990s - down sharply from a mid-2010s average near 4.0 million tons and from approximately 2.9 million tons in 2024. Vineyard removals, deliberate crop thinning, and adverse weather all contributed. In many cases, growers left grapes unharvested because buyers were unwilling to pay above cost.

While financially painful, the reduced harvest prevented further accumulation of surplus wine. Combined with smaller 2022 and 2023 vintages, the dramatically light 2025 crop is expected to bring inventory-to-sales ratios closer to normal by late 2026. Certain categories - such as Central Valley Chardonnay and Cabernet - remain oversupplied entering the year, but the overall trajectory is improving. Fewer forced discounts and fire sales are expected than in 2024-2025.

The balance remains fragile. A large 2026 harvest could reverse progress if demand fails to recover, while another light crop could tighten availability by 2027. Climate variability remains a key risk to equilibrium.

Analyst and Bank Perspectives

Industry outlooks reinforce a cautious stance. Silicon Valley Bank characterizes the current period as a “demand-driven reset unlike any in the last 30 years,” emphasizing that recovery will not come solely from supply adjustment. Consumer behavior has structurally shifted, and demand growth may take years to rebuild.

BMO Capital’s Wine Market Outlook offers a measured counterbalance. It notes that distributor inventories were finally declining by late 2025, opening the possibility of selective restocking in the second half of 2026 if economic conditions stabilize. BMO also highlights the importance of interest rate relief; potential rate cuts in late 2026 could ease financing costs and improve confidence heading into 2027. Until then, conservative purchasing is expected to persist across the supply chain.

Outlook

The economic outlook for the U.S. wine market in 2026 can be summarized as cautiously steady. Volume decline appears to be slowing, with a credible chance of stabilization by year-end. Value growth will continue to be driven by premium segments and pricing rather than renewed consumption.

For wineries, the strategic implication is clear: plan for a slow-growth, high-cost environment. Avoid overproduction, manage inventories tightly, and focus investment on segments and consumers that are still expanding. A macroeconomic tailwind could emerge, but the prudent assumption is equilibrium - not rebound. Those who adapt to the new demand reality will be positioned for resilience. Those waiting for a return to pre-2019 volume dynamics are unlikely to be rewarded.

Shifting Consumer Dynamics

The most consequential shifts in the U.S. wine market entering 2026 are not limited to tariffs or macroeconomics. They are rooted in consumer behavior: who is drinking, how often, and what wine competes with in a rapidly expanding beverage ecosystem. The American wine drinker is changing. Baby Boomers - the cohort that helped power wine’s mainstream rise in the 1990s and 2000s - are aging out of peak consumption. Millennials and Gen Z, shaped by different cultural cues, beverage preferences, and wellness norms, are not replacing Boomer volume at the same rate. Overlay the accelerating health-and-wellness movement - Dry January, sober-curious lifestyles, low-carb and “better-for-you” decision-making - and wine faces a more complex demand landscape than it has in decades.

.webp)

Evolving Demographics: Millennials, Gen Z, and Aging Boomers

The generational handoff is now the defining structural issue for wine demand. Baby Boomers (born 1946-1964) are largely in their 60s and 70s and still account for a disproportionate share of wine spending, particularly in premium categories. But their consumption is gradually declining. Some are moderating for health reasons; others simply drink less frequently with age, and every year reduces the cohort through natural attrition. Their brand loyalty also remains strong - often anchored in decades-long habits around familiar Napa Cabernet, oaky Chardonnay, or established labels. That loyalty provides stability for legacy brands, but it limits Boomer responsiveness to innovation and makes them less receptive to new formats or trend-driven offerings.

Gen X (born 1965-1980) is smaller than the Boomer cohort but occupies the “peak earnings” life stage, making them an economically important bridge generation. They drink wine, but they have not fully filled the Boomer volume gap. That reality places heightened strategic weight on Millennials and the legal-drinking-age segment of Gen Z.

Millennials (born 1981-1996; mid-20s to early/mid-40s in 2026) remain wine’s most plausible near-term opportunity - yet they are also highly contested by competing categories. This cohort came of age alongside the craft beer and craft spirits boom and tends to maintain a broad repertoire: an IPA, a go-to bourbon, summer RTDs, and occasional wine, rather than strong identity as “wine drinkers.” The upside is that Millennials often engage with wine when it’s presented with relevance and personality. They’re generally more exploratory than Boomers, seeking new varietals and unfamiliar regions, and they respond to authenticity - organic or biodynamic practices, a meaningful social cause, or a distinctive winemaker narrative.

The downside is that many Millennials are price-conscious and less loyal. Having entered adulthood during or in the shadow of the Great Recession, carrying high student debt, and navigating uneven economic growth, a $20+ bottle can feel like an occasional treat rather than a weekly staple for a large portion of this cohort. The big question for 2026 is whether Millennials “settle” into wine as they age into their 30s and 40s - historically the period when wine becomes more routine via home entertaining, family life, and food-centered occasions. Early evidence suggests some are adopting wine more consistently, but competition remains intense: craft cocktails on-premise, microbrews and RTDs off-premise, and an increasingly sophisticated non-alcohol landscape.

Millennials are not monolithic. Older Millennials (in their 40s) often behave more like Gen X in purchase patterns and brand habits, while younger Millennials (around 30) increasingly resemble Gen Z in platform usage, cultural cues, and moderation norms. Treating “Millennials” as one homogeneous segment is increasingly ineffective.

Gen Z (born 1997-2010; legal-drinking-age consumers roughly 21-28 in 2026) presents a deeper structural challenge. This cohort has been shaped by wellness culture, social media, and a measurable decline in alcohol consumption among young adults. Multiple studies and surveys show Gen Z drinks less alcohol than Millennials did at the same age. Many abstain or drink infrequently; when they do drink, they more often choose spirits, RTDs, or craft beer than wine. Wine faces a perception problem here: it can read as old-fashioned, elitist, or less fun compared with canned cocktails, seltzers, or trend-driven spirit-based drinks.

Silicon Valley Bank has explicitly warned that the majority of 20-somethings choose beer or spirits over wine, and that waiting for them to “age into” wine is increasingly risky without deliberate repositioning. A Forbes report on 2025 trends underscored the broader context: total U.S. beverage alcohol consumption was down about 3% in the first half of 2025, driven largely by declines among the under-30 demographic. Within that smaller alcohol “pie,” wine’s share is under sustained pressure.

Still, Gen Z is not inherently anti-flavor or anti-experimentation. Their adoption of hard kombucha, spiked hybrids, non-alcohol cocktails, and novel RTDs suggests they will engage when products feel culturally current and aligned with their values. This is why some wine brands are testing new formats - canned spritzers and wine-adjacent products - and leaning into values-forward storytelling, including sustainability and inclusivity, to refresh wine’s image. For wine to earn attention from Gen Z, it must feel approachable, less formal, and embedded in social occasions they actually attend. That can mean more festival relevance, pop-culture collaborations, lighter styles that align with contemporary palates (juicy chilled reds, off-dry aromatic whites), and brand language that removes intimidation.

Boomers remain essential - but are inevitably shrinking. They still anchor wine clubs, mailing lists, and fine-wine purchasing. Their frequency is tapering, and some are “trading down” as consumption declines or budgets tighten on fixed incomes. Yet wealthy Boomers continue to support ultra-premium wine for special occasions and collections, including auction-market participation.

The aggregate implication is blunt: as Boomers reduce consumption, there are not enough younger consumers stepping up at equivalent volume. Gen X and older Millennials partly fill the gap, but younger Millennials and Gen Z do not fully replace it - one reason volume decline has persisted despite premiumization.

Health and Wellness: Neo-Prohibition, No/Lo Growth, and “Better-for-You” Wine

Layered onto demographic change is a cultural shift toward health and wellness that is reshaping how often consumers choose alcohol - and whether wine retains “default” status at everyday occasions.

The “everyday drink” is weakening. The long-running narrative that a nightly glass of wine is harmless - or even healthy - has lost authority in mainstream culture. Media coverage increasingly links even moderate alcohol use to health risks. Canada’s 2023 guidance recommending no more than two drinks per week (to minimize health risk) became a widely cited flashpoint. While U.S. guidelines remain at up to one drink per day for women and two for men as “moderation,” consumer perceptions have shifted. More people - especially under 40 - are reserving wine for weekends and special occasions rather than treating it as a daily staple.

The No/Lo category continues to expand rapidly. By 2025, the global no/low-alcohol beverage market surpassed $11 billion, with projected compound annual volume growth of roughly 7% from 2022 to 2026. The U.S. is expected to see double-digit annual growth in no/low volumes over the next few years. Notably, IWSR forecasts that zero-alcohol beverages will drive more than 90% of category growth through 2026 - suggesting polarization toward either full-strength or alcohol-free, with less emphasis on “middle” low-alcohol options. Wine is a partial exception: low-alcohol wines (roughly 6-9% ABV) retain a niche, especially in styles like Moscato, off-dry Riesling, and new “light wine” products targeting health-conscious consumers. But momentum is strongest in non-alcoholic wines that aim to replicate the experience without ethanol, enabled by improved dealcoholization methods such as vacuum distillation and reverse osmosis.

Traditional wine brands are also chasing “better-for-you” cues: low sugar, keto-friendly dryness, organic/biodynamic certification, vegan-friendly winemaking, and in some cases voluntary calorie transparency. Some also market “lower sulfite” or additive-free positioning, sometimes implying fewer negative effects, though claims can drift into dubious territory. Regardless, transparency - ingredients, nutrition, farming practices - is becoming a competitive signal, especially as Europe moves toward mandated ingredient and nutrition disclosure via QR code, raising the likelihood of similar expectations migrating to U.S. consumers.

Meanwhile, moderation is changing habits. Dry January and similar programs now create predictable dips and behavioral resets even among regular drinkers. Consumers are also spacing drinks, alternating with non-alcohol rounds, and reducing total drinking occasions.

Lifestyle Shifts: Where and Why Wine Competes

Broader lifestyle changes compound these pressures. Hybrid and remote work reshaped on-premise routines: fewer after-work drinks, more home-based occasions, and an on-premise rebound that still trails 2019 in many markets. When consumers do go out, they increasingly seek curated experiences - flights, story-driven selections, wine cocktails, and programs that feel fresh rather than transactional. Wine-on-tap is gaining traction for practical and sustainability reasons: less waste, lower spoilage risk, and more flexibility to rotate interesting by-the-glass options.

Finally, wine’s competitive set is broader than ever: craft beer, RTDs, canned cocktails, hard kombucha, and in many states, legal cannabis competing for “share of buzz.” Add social media dynamics - where cocktails often dominate visual culture - and wine must fight harder to feel culturally current. The path forward is not to lecture consumers into wine, but to meet them where they are: formats, platforms, values, and occasions that match modern life.

In 2026, the consumer is younger, more health-aware, digitally influenced, and confronted with abundant alternatives. Wine can still win - but only by becoming more accessible, more transparent, more experience-led, and more aligned with the lifestyles consumers are actually living.

Premiumization vs. Value

Premiumization remains one of the clearest through-lines in U.S. wine: consumers are buying fewer bottles, but skewing toward higher-priced, higher-perceived-quality choices - while the lowest-priced segment continues to erode. That pattern held through 2024-25 and is set to persist in 2026. What’s changing is the market’s shape. The bottom is collapsing, the top is resilient, and the “middle” (roughly $9-$15, with spillover up to ~$20) is under the most pressure. In practice, wine is becoming more fragmented: a shrinking commodity end, a growing margin-led premium core, and an ultra-premium tier that operates almost like luxury goods.

The New “Entry-Level”: The Retreat of Sub-$10 and a Higher Baseline

It is increasingly hard to build a volume story around $5-$8 wines. Sales patterns in 2024-25 show the sub-$10 category shrinking sharply; many retailers report double-digit declines under $8, and softness extending into $8-$11. Several forces are driving the shift upward:

First, consumer psychology has moved. Younger buyers, in particular, often associate “cheap wine” with low quality or inauthenticity - whether that’s justified or not. They are more likely to spend a bit more for a bottle that signals credibility: a story, a sustainability cue, better packaging, a recognizable place, or simply a look and feel that doesn’t read “bargain basement.” Many producers and retailers now describe $12-$15 as the effective entry point for Millennial shoppers and newer drinkers. Below $10 tends to be perceived as “jug wine territory” unless it’s a known legacy brand or a temporary promotion.

Second, the economics of making and moving wine have reset. Higher costs for glass, closures, freight, and labor have squeezed margins to the point where many producers can’t profitably sustain a $6 shelf price. That has accelerated SKU rationalization: wineries are discontinuing low-end labels, raising prices, or concentrating effort in mid-tier and above. On the supply side, the industry is also adjusting vineyard inputs. California, especially the Central Valley, is in the process of reducing acreage tied to low-priced grapes. OhBEV’s analysts have suggested roughly 30,000-50,000 acres may need to be removed to better balance supply with demand. As those vines are pulled or shifted to other crops, cheap-wine volume shrinks further - reinforcing the new, higher baseline.

Third, channel priorities have shifted. Retailers and distributors increasingly dedicate energy to segments that deliver more dollars per unit and faster turns. That means less shelf space for 1.5L jug brands and “bottom shelf” labels, and more attention to premium 750ml bottles and trend-led categories. Where super-cheap wine still sells at scale, it’s often dominated by private label (Trader Joe’s, Costco, etc.) and a few national giants (e.g., Barefoot). The result is a bifurcation: sub-$7 is increasingly a scale-and-control game (retailer brands and a handful of mega-brands), the $8-$12 band is thinning, and then the market becomes more vibrant again above $12.

Trade policy is adding lift to this “new entry level,” too. With EU imports carrying a 15% duty in late 2025/early 2026, many European wines that once reliably hit $9.99 are now $11.99-$12.99 - pushing them out of sub-$10 by default. This has helped normalize the idea that $12-$15 is “normal” for a decent bottle, and some observers argue $15-$20 is starting to feel like the new psychological equivalent of $10 did a decade ago.

For wineries, the opportunity is to treat $12-$15 as a true on-ramp: better grapes, cleaner positioning, upgraded design, and credible claims (organic, sustainable, etc.) that make the buyer feel smart. The challenge is that everyone is moving into the same arena. Raising price without delivering a noticeable step-up in perceived value invites substitution - especially when a craft beer four-pack or an RTD option can compete at the same spend.

The Mid-Tier Squeeze ($10-$20): A Value Proposition Problem

Despite premiumization, most consumers aren’t buying $30 wine regularly. The mid-priced segment ($10-$20) remains large - but it’s caught between two gravitational pulls. On one side, price-sensitive shoppers trade down to private label, promotions, or alternative categories. On the other, aspirational buyers trade up: fewer bottles, but nicer ones. The consequence is a hollowing-out dynamic:

- The ~$9-$12 zone tends to decline unless the brand has strong recognition or a compelling external signal (ratings, awards, a clear origin story).

- The $12-$18 range is crowded and often flat; growth tends to accrue to brands with distinctiveness rather than broad category lift.

- Momentum becomes more visible as you approach $20+, where “premium” begins to feel meaningfully differentiated.

Mid-tier brands are responding by trying to make value legible again without becoming “cheap.” That generally shows up in a few forms: refreshed branding and storytelling; quality upgrades aimed at credible third-party validation (e.g., 90+ point scores); promotion mechanics that feel like a deal without undermining the brand; and alternative packaging that improves the per-glass economics while keeping quality perception intact. A notable niche is the “premium box”: 3L formats priced around $20-$30 that deliver a per-bottle equivalent of $5-$7 while positioning the liquid closer to what consumers expect from a ~$12 bottle.

The strategic task for 2026 is clarity of use-case. Mid-tier cannot win by being vaguely “good for the money.” It needs a job: a reliable Tuesday-night bottle, a host gift that won’t look cheap, a fridge staple that pairs with real food, or a repeatable house wine with enough personality to feel intentional.

Premium Strength ($20-$50): Trading Up and “Less, but Better”

The premium band is still the industry’s most dependable growth engine in value terms. Even as overall volume has struggled, $15-$50 wines have generally held up better - supported by consumers who drink less frequently but want a better experience when they do. That “less but better” mindset is reinforced by on-premise behavior as well: wine lists skew toward higher-quality selections, by-the-glass programs increasingly support premium pours, and preservation systems allow consumers to access higher-tier wines without committing to full bottles.

Direct-to-consumer also plays a role. Wineries have pushed premium through clubs, limited releases, and allocations, and average shipment prices rose to record highs in 2025 - momentum that is likely to persist in 2026 as DTC continues to skew upmarket.

The caveat is competition. At $25, consumers have enormous choices: domestic wines from emerging regions, compelling imports (even with tariffs), and premium-adjacent alternatives like high-end craft beer or RTDs. That makes brand building - story, consistency, trust - more important than ever.

Ultra-Premium and Collectible Wines ($100+): A Different Market

At the top end, wine behaves less like FMCG and more like luxury collectibles. Cult Napa Cabernet, top Burgundy and Bordeaux, prestige Champagne, and trophy allocations are purchased by affluent enthusiasts and, increasingly, by buyers who treat fine wine as a collectible asset. This segment was notably insulated in 2025 and is likely to remain stable or rise modestly in 2026, supported by high-net-worth spending and the continued emphasis on exclusive experiences: private tastings, VIP lounges, member-only events, and travel-driven hospitality that deepens loyalty.

Prices at the top are not immune to reality - there have been signs of secondary-market corrections in certain regions after overheated peaks - but the dominant pattern remains brand-led pricing power and experience-led retention. International demand can amplify this, making top-tier wines increasingly global commodities.

What This Means for 2026

The market is splitting into distinct games: a shrinking commodity volume game at the low end, a margin and loyalty game in premium, and a luxury experience/collectible game at the top. Mid-tier is stuck in between unless it can articulate value in a sharper, more modern way.

In practical terms: sub-$10 keeps contracting, $10-$20 must earn relevance, $20-$50 drives revenue growth, and $100+ remains brand- and experience-driven. Premiumization is not a fad in 2026 - it’s the operating condition of the category.

What’s Hot, What’s Not

Consumers aren’t just changing how much wine they buy - they’re changing which wines (and wine-adjacent formats) they reach for. Across 2025 and into 2026, the pattern is consistent: whites and rosés are gaining share, many reds are soft, sparkling continues to outperform (with some trade-down dynamics), and No/Lo plus alternative formats (cans, kegs, Tetra Pak) are widening wine’s “occasion map.” At the same time, curiosity is rising for lesser-known varietals and emerging regions, especially among Millennials and Gen Z, who often discover wine through restaurants, indie shops, and social media rather than traditional “varietal loyalty.”

Whites and Rosé Keep Rising; Reds Face Structural Headwinds

White wine momentum remains one of the clearest shifts. Varietals such as Sauvignon Blanc, Pinot Grigio/Pinot Gris, Albariño, and Chenin Blanc are pulling demand, with Sauvignon Blanc singled out as a standout - New Zealand Sauvignon Blanc imports continue climbing, and domestic plantings in California are increasing to meet consumer interest. The demand drivers are straightforward: whites are widely perceived as more approachable (lower tannin, served chilled), more refreshing, and more food-flexible - especially with the kinds of meals that have grown more common (salads, sushi, vegetarian fare). There’s also a “lighter” perception (body/calories), whether perfectly accurate or not, and perception matters at shelf. Chardonnay still dominates by volume, but its growth is broadly flat compared to the surge in crisp/aromatic whites.

Rosé has proven it’s not a fad. The late-2010s “rosé boom” has normalized, yet rosé remains among the healthiest wine segments. In 2025, rosé was described as up slightly in volume and more in value as consumers trade into premium rosés from Provence, California, and other origins. Rosé has also become more year-round (even if summer is still the peak season). For 2026, the expectation will continue growth - not explosive, but steady, potentially mid-single-digit volume gains - with competition increasing as more producers launch rosé SKUs and overall quality rises. A notable subtrend is sparkling rosé, which stacks two growth vectors (pink + bubbles) into a single proposition.

Meanwhile, red wine is under pressure, particularly heavier styles and sweet-leaning reds. The “big red blend” craze that drove large volumes a decade ago has cooled; consumers are either moving up into more serious single-varietal reds or shifting to other categories. Even staples like Merlot and Cabernet Sauvignon show softness in lower-priced tiers, while premium Cabernet remains strong among collectors and Pinot Noir holds up better among enthusiasts. This is a generational palate shift: younger drinkers leaning toward lighter, brighter, more acid-driven profiles over oaky, tannic, higher-alcohol reds that aligned with Boomer/Gen X preferences. Moderation and wellness cues also matter - reds are often perceived as heavier and higher ABV, which can clash with a “mindful” consumption mindset.

A key nuance: red isn’t disappearing; it’s re-orienting. There’s a rising interest in lighter reds - especially Pinot Noir, plus increasing attention to Gamay (Beaujolais) and “chillable red” culture. Certain wine bars report that chilled reds are becoming fashionable among younger guests, and the natural-leaning “glou-glou” trend (gulpable, low-tannin reds often using carbonic maceration) is pulling adventurous Millennials and Gen Z. That trend also connects to “craft” cues - playful labels, lower formality, and a vibe closer to craft beer.

Broader lifestyle forces reinforce the shift: changing eating patterns toward lighter, plant-forward cuisine, and the reality of warmer weather pushing consumers to refreshing whites and rosés. The implication for producers is operational: some wineries are repurposing fruit once destined for red blends into rosé programs; there’s increased planting and focus on whites (e.g., Sauvignon Blanc, Albariño, Rhône whites like Marsanne/Roussanne). For red-focused brands, the strategic response is to emphasize what removes friction - elegance, freshness, moderate alcohol, restrained oak, and/or organic and ingredient-forward cues.

Sparkling Wines: Strong Growth, With Trade-Down Within Bubbles

Sparkling continues to align with modern consumption: “everyday celebration,” shareability, and social-media-friendly rituals. Sparkling breaks into value-driven fizz, Champagne, and broader “other bubbly” growth.

Prosecco remains the mass-market engine: crowd-pleasing profile, accessible pricing, and a celebratory signal without Champagne’s cost. U.S. imports hit all-time highs in 2024 and kept rising in 2025, with continued momentum expected into 2026 (possibly at slower growth rates simply due to scale). Prosecco Rosé (authorized in 2020) added incremental energy by combining rosé appeal with bubbles and is performing well, especially with younger consumers. Cava is also growing, more quietly, positioned as a drier, more “wine-like” value alternative (traditional method) often under $15.

Champagne is more nuanced. After booming in 2021-22, supply constraints and price increases moderated demand, and the 15% U.S. tariff in 2025 added further pressure. The Champagne volumes in the U.S. dipped in 2025, especially entry-level non-vintage, as consumers balked at higher shelf prices (e.g., NV bottles rising into the ~$60 range from ~$45). Prestige and luxury cuvées held up better with affluent buyers. For 2026, the expectation is flat to slightly up volume and better value growth via mix and price, with a key swing factor: whether tariff relief arrives through a trade deal (which could reduce price pressure or at least prevent further increases). Importantly, the overall sparkling lift doesn’t require Champagne to win every occasion - many consumers are substituting Prosecco/Cava for casual needs and keeping Champagne as an aspirational purchase.

On the supply side, domestic sparkling is gaining: California, Oregon, New Mexico (notably Gruet), and emerging regions are investing in sparkling programs, and premium domestic sparklers offer a “homegrown” alternative at meaningfully lower price points than Champagne. The broader set - Crémant, Franciacorta, UK sparkling - continues to grow niche followings, while pét-nat plays an outsized cultural role in natural wine circles by attracting younger drinkers with a more experimental, craft-coded proposition.

Emerging Varietals and Regions: Curiosity as a Competitive Lever

Curiosity is becoming more central to wine discovery. Sangiovese and other Italian varietals are a growing point of interest, both through imports (e.g., a resurgence in Chianti Classico and broader Tuscan enthusiasm) and through domestic experimentation in California and Washington (with grapes like Sangiovese, Nebbiolo, Barbera). Sangiovese’s appeal is described as medium-bodied, food-friendly, and story-rich - attributes that play well in modern wine-bar culture.

Chenin Blanc is positioned as a “cool again” varietal. Once associated with older California jug-wine blends, Chenin is being revived by a new cohort of winemakers (Santa Ynez, Mendocino, Clarksburg/Sacramento Delta), influenced by the reputation of Loire Chenin (Vouvray) and the export success of South African Chenin. Its versatility, acidity, and moderate alcohol align with “food-friendly” and “mindful” trends.

Other underdog grapes noted include Gamay (especially in Oregon as a lighter red option), Grenache (brighter, pinot-like expressions), Grüner Veltliner (small U.S. plantings aiming at crisp-white fans), and even experimental work with Assyrtiko. Natural wine continues to introduce consumers to grapes like Mission (Pais), Trousseau, Counoise, plus field blends - shifting the cultural frame of “blend” from mass-market concoction to heritage/curated craft.

Emerging U.S. regions matter less for national volume and more for narrative power and local pride: Texas (Tempranillo, Tannat, Viognier; tourism-led growth), Virginia (Viognier, Cabernet Franc), New York (Finger Lakes Riesling, cool-climate reds like Cabernet Franc), plus Michigan/Ohio/Maryland, Arizona/New Mexico, and Idaho’s Snake River Valley. These regions reinforce a “craft and local” identity that resonates with younger consumers and supports wine tourism and local retail ecosystems.

No/Lo, Alternative Formats, and Hybrids: Wine Expands Its Territory

The low/no-alcohol wines are moving from fringe to tracked category status. NielsenIQ is referenced as tracking non-alcoholic wine separately and reporting large percentage increases (from a small base). This is drawing in wineries that previously avoided dealcoholized products, either by building programs or partnering with specialized producers.

At the same time, alternative packaging continues to reshape occasions: cans, Tetra Pak, kegs bring wine into contexts where it historically underperformed (beach, festivals, convenience-led single-serve). Canned wine is described as still a small share of total wine but growing - high single digits in 2025, with expectations of continued growth in 2026, often concentrated in spritzers and rosé styles.

Finally, the flavored and hybrid wine-based beverages - wine aged in whiskey barrels, Moscato-based flavored extensions, botanical additions, tea-wine fusions - are a way to compete for flavor-seeking consumers who migrated toward hard seltzer and RTDs. Traditionalists may dismiss these, but they can recruit consumers into the wine universe and expand the category’s relevance.

Bottom line: the American wine palate is broadening. Core varietals still dominate, but the margin - and future - often sits in the “edges”: whites/rosé growth, sparkling trade-down flexibility, lighter-red culture, experimentation with grapes and regions, and formats that fit modern life. The winners in 2026 will be those that either participate directly in these rising pockets or position their flagship styles in ways that match where consumer taste is heading.

Distribution, On-Premise, and DTC Channels

The “how” of wine sales is still recalibrating after a half-decade of shocks: pandemic-era channel whiplash, distributor consolidation, oversupply, e-commerce normalization, and a hospitality landscape that’s more experience-led than ever. In 2026, the three-tier system remains the backbone, but it operates with leaner inventories and tighter SKU discipline; on-premise is recovering unevenly while innovating fast; and DTC has settled into a new baseline that is smaller than the COVID peak but structurally more important than pre-2020 - especially in value terms.

Inventory Reset and Oversupply: Channel Behavior Is Still “Lean First”

The oversupply story isn’t just a winery problem - it reshaped the entire pipeline. Going into 2025, many distributors were holding too much wine relative to demand, driven by optimistic ordering in 2019-2020 and subsequent consumer softening. That imbalance triggered a multi-year “inventory discipline” phase that affected which brands got attention and how fast new items could earn placements.

Distributors responded with tight replenishment behavior in 2024-25, buying cautiously and prioritizing proven movers. Brands that didn’t turn quickly were deprioritized or dropped, and smaller wineries found it harder to secure new placements because wholesalers were already “loaded.” Retailers, especially chains, also reacted to slower turns by rationalizing SKUs, trimming redundant or slow-moving wines - most notably in sub-premium bands - and reallocating space toward faster-growing categories like RTDs and other adjacent beverages, or simply giving more facings to fewer proven performers.

By late 2025, there were signs that the overhang was finally easing. Several forces contributed: deliberate discounting and targeted sales pushes to clear older stock, plus the supply-side relief from a lighter 2025 harvest, which reduced the volume entering the pipeline. Wineries also used tactics to offload excess without destroying flagship pricing: closeout deals tied to distributor incentives, private-label one-offs for flash-sale sites, and exports into low-visibility channels. The bulk wine market, which had been extremely active in 2020-2024, also cooled; some unsold bulk was distilled, destroyed, or redirected into industrial uses to avoid indefinite storage costs - painful, but a mechanism for preventing the glut from compounding.

For 2026, the practical outcome is a healthier inventory picture and less desperation pricing. Promotions will remain part of wine’s DNA, but the “constant deep discount” environment should be less intense if inventories truly normalize. One important nuance is the possibility of a mild restocking effect: if distributors and retailers depleted aggressively in 2025 to right-size, they may step up orders in 2026 to rebuild working stock. That can temporarily make winery shipments look stronger than consumer off-take, so interpreting 2026 shipment data requires caution - some uplift may reflect channel refill rather than demand acceleration.

The bigger strategic implication is behavioral: even when inventory levels normalize, the industry may retain the learned habit of operating lean. Just-in-time feels safer than loading up, especially in a market where demand growth is not guaranteed.

On-Premise: Uneven Recovery, Stronger Experience Economics

On-premise remains pivotal for premium wines and brand building, and it’s still climbing back from 2020’s collapse. 2025 was an improvement year - more people returned to dining out - yet several structural drags kept on-premise below 2019’s volume peak: business travel and conferences not fully normalized, more takeout and casual occasions, and restaurant cost inflation plus staffing challenges that forced streamlined operations and higher by-the-glass prices.

As of early 2026, the estimate given by our analysts is that on-premise wine volume is roughly 85-95% of 2019, varying by region and segment. Fine dining in major metros may be close to full recovery (affluent guests returned to high-ticket wine occasions), while casual chains can lag if their core customers remain price-sensitive.

What’s most notable is how quickly restaurants and bars have modernized their wine programs to fit today’s guest psychology - less commitment, more discovery, more story, and more perceived value:

- Curated, slimmer lists are replacing “phone-book” inventories. Many operators want fewer SKUs they can actually sell with confidence, and they often favor distinctive, narrative-rich wines (orange wines, natural selections, niche domestic regions) that help the venue stand out and give staff something interesting to talk about.

- Stronger by-the-glass (BTG) programs reduce friction for groups with varied tastes and for guests who don’t want a full bottle. Tools like Coravin support premium BTG offerings, including rotating “reserve” pours that let diners taste expensive bottles by the glass.

- Wine on tap continues expanding, especially in casual and bar-centric openings. Keg wine lowers cost-per-ounce, reduces spoilage, supports sustainability messaging, and enables half-pours and flights more easily - making wine feel more “approachable” in the same way craft beer taps do.

- Flights, pairing menus, and education-led experiences are increasingly used to drive engagement and revenue. Even if total volume per guest is moderate, the number of wines tasted can rise - and the experience commands premium pricing.

- Casualized service and storytelling are replacing old sommelier stereotypes. The sales pitch becomes human and values-led (“organic practices,” “only 12% alcohol,” “revived old vines”), aligning with post-pandemic dining preferences and younger consumers’ desire for authenticity.

- Pricing strategies are adapting to sticker shock. Some venues use scaled markups - higher on cheaper wines, lower on expensive ones - to move better bottles; others rely on happy hours and weekday specials to keep wine accessible.

For wineries, the on-premise channel remains one of the best “trial engines.” A glass discovered at a restaurant can translate into retail purchases or DTC signups. That makes support tactics in 2026 especially important: BTG-friendly pricing and placements through distributors, staff education, winemaker dinners and pairing events, and programs that help restaurants tell the story with confidence. There’s a lane for smaller producers: independent restaurants often prefer unique picks and avoid labels that guests can buy anywhere, so the high-energy part of on-premise is often the most open to discovery.

DTC and Digital: Smaller Than the Peak, More Strategic Than Ever

DTC surged during the pandemic, then normalized as tasting rooms reopened and consumers shifted habits. The key distinction - volume versus value: shipment volumes came down, but the average price per bottle shipped reached new highs, meaning DTC’s importance has grown disproportionately in revenue and margin terms.

Using SOVOS/ShipCompliant as the reference, 2024 was a year where DTC volume dropped (often cited as roughly 5-10%) while value held steady or rose slightly due to higher price points. By 2025, the decline slowed, suggesting a new baseline. For 2026, the expectation is roughly flat DTC volume with modest value growth - the “COVID bump” is gone, but DTC remains structurally larger than pre-2020 and more central to premium strategy.

Tasting rooms show a similar pattern: visitation was still below 2019 in 2023-24, with reasons ranging from travel shifts to demographic change and the widespread adoption of reservation-only models and high tasting fees. Napa-style tasting fees of $50-$100 are positioned as a barrier for younger or newer consumers; some wineries are trading volume for higher revenue per visitor. 2026 will bring a split approach: ultra-premium wineries will keep high-touch paid experiences, while mid-tier operators may experiment with more accessible pricing or walk-in friendliness to rebuild foot traffic - because visitation is still a key driver of club growth and case sales.

Wine clubs remain the DTC spine, but the playbook is evolving. Subscription fatigue and competition mean wineries are focusing less on “set-and-forget shipments” and more on tiering, perks, and community: multiple club levels, access to library wines, exclusive events, virtual tastings, and digital member experiences that deepen loyalty. Some smaller wineries also lean on third-party platforms that help manage compliance and shipping complexity.

Digital commerce is no longer just “winery websites.” There’s a broader ecosystem of online retailers and marketplaces - Wine.com, Vivino’s marketplace, local delivery platforms - and Winc’s 2022 bankruptcy is proof that growth-at-all-costs didn’t work. For producers, these platforms can be both competition and distribution: many brands still prefer direct margins and data ownership, but consumers buy where convenience and selection are best, so wineries increasingly monitor and manage presence, pricing, and brand representation across these channels.

E-commerce has also become more “three-tier enabled.” Local shops and distributors strengthened their online ordering and delivery capabilities during lockdowns, and consumers now treat that convenience as standard. That blurs the lines between DTC and retail e-com - yet from a brand standpoint, it means product content, imagery, and storytelling must work everywhere a consumer encounters the bottle.

Regulation remains the backdrop constraint. Winery shipping is allowed to most states, though it’s still a patchwork. Retailer shipping across state lines remains highly restricted, with ongoing legal and legislative discussions that could reshape the digital playing field if they move in a more permissive direction.

The operational bottleneck for DTC remains shipping economics: adult signature requirements and carrier costs can make case shipping expensive, forcing wineries to subsidize or waive shipping thresholds and protect margin through bundling. There were continued tactical responses: encouraging 6- or 12-bottle buys, using closer fulfillment centers, exploring regional warehousing, and experimenting with lighter packaging. Sustainability concerns are emerging here too - packaging waste and carbon footprint are increasingly visible to eco-conscious buyers.

The 2026 Reality: Omnichannel or Bust

The throughline in 2026 is integration. The most resilient brands treat wholesale, on-premise, tasting room, and online as connected touchpoints: restaurant discovery feeds retail pull and DTC signup; tasting room feedback informs what works in the market; distributor placements create visibility that supports direct storytelling. Consumers move fluidly across channels, so brand consistency - clear positioning, strong product truth, and coherent messaging - matters as much as the channel mix itself.

Industry Consolidation and Competition

The U.S. wine industry has always been a “long tail”: a small group of giants controlling a large share of volume, and hundreds of smaller wineries competing for attention, placements, and direct relationships. What’s changed in the last few years is the speed at which pressures - oversupply, volume softness, rising costs, and tariff uncertainty - have pushed the market toward consolidation. At the same time, wine’s competitive set has expanded beyond “other wine brands” to include RTDs, spirits, hard seltzers, non-alc alternatives, and cannabis in legal states, all vying for the same shelf space and consumer occasions. The net effect in 2026 is a tougher, more gatekept market: fewer, larger intermediaries; tighter retail planograms; and a sharper need for wineries to choose between scaling up or specializing.

Winery Mergers, Acquisitions, and Closures

The strain has been most acute for small and mid-sized wineries that depend on tasting room revenue plus local distribution. When the oversupply cycle intensified and distributors tightened buying, many smaller producers found themselves squeezed from both sides: too much inventory and too little pull-through at wholesale. Layer in cost inflation - labor, farming, compliance - and the result has been a clear wave of exits and consolidation.

A notable casualty has been the “virtual winery” model (brands without estate vineyards or facilities, buying grapes and renting production). Virtual brands are easy to launch in boom times, but also easy to shutter when demand softens and customer acquisition becomes expensive. Many virtual labels quietly disappeared in 2024-25, often because they lacked a durable point of difference. In 2026, plenty of labels still look “independent,” but many sit inside larger portfolios; the truly independent set increasingly lives either in a tight local niche or a DTC-only lane.

On the acquisition side, consolidation has continued across large strategics, mid-size groups, and private capital. The major companies continue to buy brands and assets to strengthen premium portfolios - for example, E.&J. Gallo picking up brands from smaller family wineries (often for inventory, vineyards, or production assets), while Constellation Brands - after shedding lower-end labels earlier - remains oriented toward higher-end positioning and could selectively add niche luxury producers. Private equity also remains active, attracted by depressed valuations in a low-growth cycle and the ability to “roll up” assets, streamline operations, and expand margins. There’s an ongoing reorganization of Ste. Michelle Wine Estates (acquired in 2021) - an example of how investment owners can restructure platforms and potentially pursue bolt-on growth.

Beyond headline M&A, consolidation is also showing up as “shared infrastructure” among mid-sized operators. The idea is simple: in a market where demand is not reliably expanding, pooling back-office functions (compliance, accounting, certain production or logistics tasks) can preserve brands while reducing overhead - essentially “synergy through scale” without fully collapsing labels into one identity. This is especially relevant for regional clusters (e.g., multiple Sonoma producers) that can keep label separation while sharing cost centers.

Vineyard consolidation adds another layer. The piece notes two simultaneous dynamics: (1) lifestyle or investment buyers purchasing vineyards and potentially taking them out of traditional commercial channels (sometimes selling grapes selectively rather than operating a full-scale winery), and (2) vineyard removals, particularly in California’s Central Valley, where marginal acreage is being pulled to address demand collapse at the low end. 30,000-50,000 acres may need to come out to rebalance the market, and also roughly 10% of CA acreage could be pulled in this cycle. This is consolidation by subtraction: fewer growers, fewer “commodity” supply sources, and (eventually) more balanced inventories that benefit survivors - though at significant near-term pain for growers.

All of these factors reinforce the scale logic. In a low-growth environment, one reliable route to expansion is acquisition - buying market share rather than waiting for organic category growth. Big companies can spread distribution, marketing, and compliance costs over more cases, improving efficiency and bargaining power. By 2026 the top 10 wine companies will account for an even larger share of U.S. wine volume - already described as likely over 70%, with potential incremental gains as brands are absorbed. Meanwhile, the number of bonded wineries may remain high (new niche entrants still appear), but more of those will stay small, local, or DTC-only - and many will eventually exit without scale or a defensible niche. The piece also flags the possibility of opportunistic international acquisitions (European or Australian groups buying U.S. assets) if valuations remain attractive, echoing prior examples of global luxury ownership in U.S. wine.

Distributor Consolidation and Shelf-Space Gatekeeping

If winery consolidation determines “who makes the wine,” distributor consolidation increasingly determines “who gets seen.” The distribution tier has concentrated for decades, and it remains dominated by two mega-distributors (Southern Glazer’s and RNDC/Young’s) across much of the country. By 2026, many states function as duopolies or triopolies, meaning a winery without a relationship inside those networks can struggle to achieve meaningful retail and on-premise penetration.

Distributor economics reinforce this. Facing margin pressure from inflation, labor, and fuel, wholesalers have reduced the number of brands and SKUs they carry, focusing on what sells and what is supported with incentives. Portfolio rationalization is especially severe post-merger: if two houses have overlapping offerings, one gets cut - typically the smaller or slower-moving brand. The net impact for wineries is fewer, larger gatekeepers and higher expectations around velocity, discounts, and program funding. Mid-size wineries feel this most sharply: not artisanal enough to thrive purely on DTC identity, not large enough to command national distributor priority. The “middle squeeze” isn’t only a price-tier story - it’s an organizational survival story.

In retail, shelf competition runs on two fronts. Inter-category, wine is losing some fridge and aisle real estate to RTDs, canned cocktails, hard seltzers, craft spirits adjacents, and non-alc beverages, as planograms follow growth. Intra-category, retailers have expanded private label and exclusive brands, which offer higher margins and greater control. Chains and big box specialists can push exclusives hard, compressing space for independent labels. Large suppliers can also buy visibility through endcaps, racks, and category management relationships; small wineries rarely have the leverage to compete on those terms.

How Wineries Route Around the Bottlenecks

The piece points to several “escape valves” that have become more important as gatekeeping tightens: self-distribution where legal, direct-to-retail relationships in local markets, stronger reliance on DTC/tasting rooms, and online platforms that reduce dependence on physical shelf. These are not universally available or easy, but they represent strategic alternatives when national distribution economics don’t pencil.

Meanwhile, wine’s competition is not only structural - it’s cultural. Spirits remain robust (including tequila and whiskey booms), beer retains craft energy and marketing budgets, and newer consumption patterns (aperitivo culture, cocktail-forward dining) compete directly with wine at the table. The industry’s defensive advantage is still food compatibility - wine as the companion to meals - but even that territory is contested as consumers pair beer or cocktails with dinner. The piece argues that wine must actively reinforce relevance through events, education, and clearer point-of-sale pairing guidance.

Labor and technology compound the consolidation advantage. Larger entities can invest in mechanization, automation, warehouse tech, and route optimization to offset labor scarcity in vineyards, production, and distribution. Smaller operators often can’t, which further tilts the playing field toward scale.

The “Barbell” Market Structure

The end-state described is a barbell: at one end, a small set of large companies controlling mass distribution with efficient production, economies of scale, and heavy promotion; at the other, many small producers serving niches through clubs, boutique shops, local restaurants, and direct relationships. The middle - regional brands without national reach and mid-size wineries without strong DTC gravity - gets squeezed or absorbed. In a large retailer in 2026, you may still see many labels, but fewer truly independent voices behind them; in a boutique wine shop, you’ll find the indie set that rarely appears in chain planograms.

The strategic conclusion is blunt: scale or specialize. Scale buys distribution power and cost efficiency; specialization buys devotion, pricing integrity, and insulation from mass-market squeeze. Many of the most resilient players do both - operating a high-volume label for retail economics while maintaining a small-lot, identity-rich tier for DTC and brand equity. In 2026, flexibility and smart alliances - whether with distributors, investors, or peer wineries - will largely determine who can navigate the consolidation cycle and the broader fight for “share of throat.”

Environmental and Policy Pressures

Wine is uniquely exposed to environmental volatility: climate affects yield, quality, timing, and cost in ways few consumer categories experience. In parallel, policy and regulation - labeling transparency, health warnings, tariffs, and shipping rules - add operational and reputational pressure. In 2026, climate impacts are increasingly visible in vineyards, and transparency/health policy discussions are moving closer to real change. Wineries that plan early (rather than react late) will be better positioned.

Climate change impacts on vineyards and harvest yields

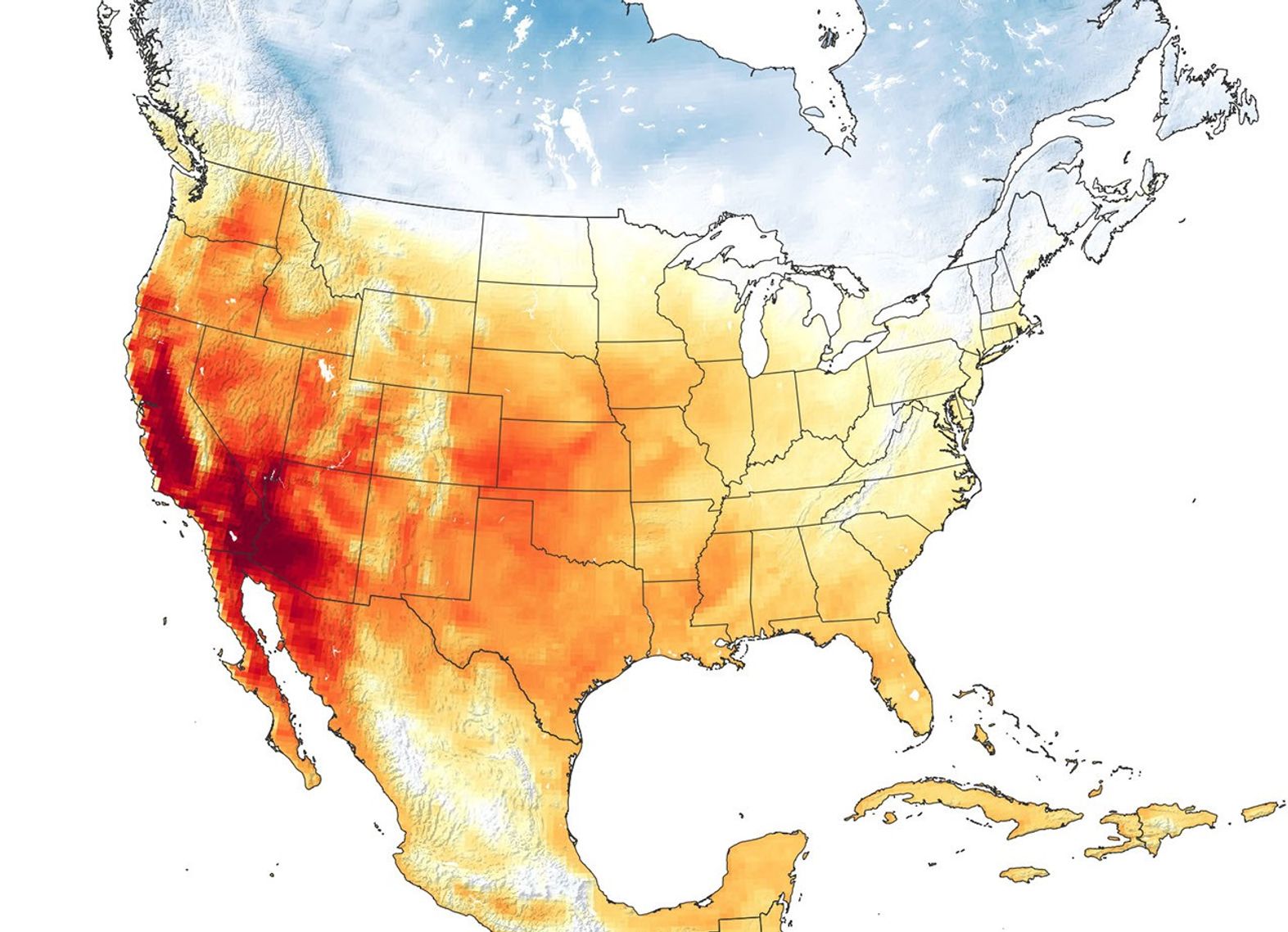

The climate challenges that have been building for years are now operational realities. Across U.S. regions, growers are managing more frequent extremes that change how vineyards are farmed and how harvest is executed.

Heat and drought. Recent years brought record heat events in major wine areas. California has experienced repeated intense heat spells (2022’s Labor Day heat wave and a very hot July in 2025 in some areas). Heat can push grapes to ripen too quickly - sugar rises faster than flavor and tannin development - creating imbalance unless growers intervene. It also increases the risk of vine stress and direct cluster sunburn. Drought remains a recurring issue, even with occasional wet years; while 2023 delivered substantial rain, the prior multi-year drought left vines stressed and yields smaller. Water availability is now a strategic constraint: some Central Coast sites faced severe rationing, and vineyards that couldn’t be sustained were removed. Looking ahead, 2026 can be among the hottest years, reinforcing the expectation of another challenging season.

Growers are responding with a set of practical adaptations, increasingly standard rather than experimental:

- Shading and canopy management: leaving more leaf cover (or using shade cloth in extreme cases) to protect fruit.

- Irrigation efficiency: expanded drip irrigation, soil moisture sensors, recycled water, and shifts toward drought-tolerant rootstocks or dry farming where feasible.

- Alternate varieties: trials of heat-tolerant Mediterranean grapes (e.g., Vermentino, Grenache, Touriga Nacional) in areas previously dominated by cooler-climate varieties.

- Higher elevation vineyard moves: pushing plantings upslope or into cooler altitude zones, while managing tradeoffs like access and erosion.

Wildfires and smoke. The West’s catastrophic fire years (late 2010s through 2021) made smoke taint a permanent risk factor, especially after 2020’s severe impacts. 2025 was comparatively fortunate, but drought conditions can bring fires back any year. This forces wineries to maintain smoke-taint playbooks: research into protective vineyard sprays, winemaking mitigation tools such as filtration approaches (carbon fining, reverse osmosis), and contingency sourcing if a region is hit. An important cost implication is insurance: wildfire insurance has become extremely expensive or unavailable in some California regions, forcing some operators to self-insure - meaning higher risk on the balance sheet. In 2026, a bad fire season would quickly test the resiliency of these systems.

Unpredictable frost and rain (“climate weirding”). Climate change isn’t only warming - it increases volatility. Unseasonal spring frosts can hit after early budbreak, damaging crops in regions like the Northwest and in “marginal” zones at high latitude/altitude. Wineries are investing in frost protection (wind machines, sprinklers) and, where possible, selecting later-budding clones or varieties. Rain volatility is equally disruptive. Heavy downpours or off-season rain can trigger mildew, rot, dilution, and harvest complications. A rainy 2025 California harvest created mold pressure and made ripeness targets harder in some grapes. Producer responses are increasingly systematic: tighter vineyard disease management, more rigorous fruit sorting, and sometimes making less wine to protect quality.

Harvest windows and labor constraints. Warmer seasons are pulling harvest earlier in many regions; fruit that used to be picked in September may now ripen in August. This compresses logistics when multiple varieties ripen at once and increases exposure to extreme heat. In high-risk heat forecasts, some growers pick earlier to avoid raisining, accepting a different flavor profile to save the crop. This all intensifies labor needs at the exact moment labor is hardest to secure. The result is accelerated interest in mechanization, especially in flatter, larger vineyards where machine harvesting is suitable. Mechanical harvesters also enable night picks, reducing heat risk and improving working conditions.

New regions and shifting “best sites.” One of the few upsides of warming is that regions previously too cool are becoming viable. The piece uses England’s rise in sparkling wine as a clear example, with climate trends making some UK zones resemble Champagne’s historical conditions. In the U.S., growers experiment further north or at higher elevation (e.g., mountain zones such as Colorado), often using hybrids in the coldest areas. Within established regions, cooler pockets and aspects gain value: north-facing slopes, coastal edges, and fog-influenced sites become prized. There’s a “hedging” behavior too - Napa producers acquiring Oregon land to diversify climate exposure.

Long-term adaptation: soil health and regenerative approaches. Beyond tactical fixes, vineyards are increasingly pursuing resilience through soil and ecosystem health. Regenerative viticulture and improved organic matter can increase moisture retention in drought years and improve vine stress tolerance. That pushes more vineyards toward organic, biodynamic, or sustainability certifications, and it increases interest in research - traditional breeding and possibly gene-editing - for heat/drought tolerance and disease resistance as pest pressures shift with climate.