.svg)

%20(1).jpg)

.gif)

Beer sales have entered a transitional phase. After pandemic-driven volatility, global beer volumes are stabilizing with moderate growth driven by events, new products, and shifting tastes. The upcoming FIFA World Cup (2026 in USA/Mexico/Canada) and other major events will drive spikes in demand. At the same time, trade disruptions and tariffs are reshaping costs and trade flows, while consumers continue moving toward premium, low-alcohol, and non-traditional options. Industry analysts forecast slow, single-digit growth in beer market value (e.g. ~4% CAGR over 2026-2032), meaning 2026 will be a “reset” year. Brewers and marketers should expect a mixed picture of slight growth in some markets, declines in others, and ample opportunities in emerging niches (craft, health drinks, sustainability).

FIFA 2026 World Cup: Shaping Beer Demand through Major Sporting Events

Major sporting events historically spur big jumps in beer consumption. For example, during the 2018 FIFA World Cup Budweiser’s marketing blitz drove a 10.1% revenue jump in key international markets and stadium beer sales exceeded those in 2014. AB InBev credits world cups for “accelerating Budweiser’s growth” in markets like China, Brazil, UK and South Africa. In Qatar 2022, Budweiser pivoted to its alcohol-free Budweiser Zero (after a stadium alcohol ban) and even salvaged a $75M sponsorship by running viral campaigns. Such examples show that well-executed campaigns - from branded fan zones and special cups to social media contests - can lift sales dramatically.

The 2026 World Cup spans 16 cities in North America (June 11-July 19, 2026) with 6.5 million spectators - roughly double the 1994 U.S. audience. In past host countries, on-premise beer volumes surged by 2.5-9.9% above normal growth rates during the tournament. Barclays predicts boosts especially in premium and low-alcohol segments as fans treat the event as a special occasion. North American venues already include many of the world’s top beer-consuming countries, so local craft and macro brewers alike should plan for heightened demand.

Beer companies should deploy fan-centric marketing: viewing parties, co-branded glassware, and local sponsorship tie-ins. Even with advertising restrictions in some venues, creative promotions (like digital fan challenges or out-of-home messaging) can pay off. Key lessons: activate around fan rituals (tailgate celebrations, watching parties, victory toasts), partner with local teams or influencers, and be ready to scale up production and logistics in Q2-Q3 2026. Brands with strong local presence (e.g. Mexican lagers in Mexican host cities, craft beers in Canadian venues) will likely enjoy an extra lift.

Global Market Outlook: Growth Regions and M&A Activity

Global beer growth is uneven. Mature markets (North America, Western Europe) show flat-to-slight declines in volume, offset by rising value through premium brands. Asia-Pacific and Latin America offer the most upside: rising incomes and alcohol consumption drive mid-to-high single-digit growth in countries like China, India, Vietnam and Brazil. For example, China’s per-capita GDP is still growing rapidly, and United Breweries in India is expanding capacity to meet 10%+ regional growth. Big brewers are investing accordingly: Carlsberg announced a $90M brewery expansion in Vietnam (2025), AB InBev increased Indian production, and Heineken is rolling out new breweries in Eastern Europe. Global beer market value was about $986 billion in 2025 and is forecast to exceed $1.3 trillion by 2032 (roughly 4% annual growth).

Consolidation remains key. Large multinationals continue M&A to gain scale and new segments: AB InBev’s 2016 merger with SABMiller created a near-monopoly (though integration has proven painful), and craft-focused groups have been acquired or merged (e.g. CANarchy to Monster Beverage). In early 2026 AB InBev even spent ~$3 billion to buy back the remaining stake in its U.S. metal-packaging plants - effectively undoing a 2020 divestiture. This move was designed to control can quality and cost amid tariffs. On the other hand, regional players are forming alliances: in the U.K., private equity roll-ups like Keystone Brewing Group have snapped up multiple craft labels.

At the same time, an emerging theme is localization. Global giants are relying on local breweries and brands to connect with regional tastes. AB InBev’s 0.0 launches and Heineken’s Champions League campaigns often feature local beers or tie-ins with city pride. Weaker brewers are divesting or shutting underperforming facilities - for instance, Molson Coors and Heineken each saw declines in some legacy brands (e.g. Dos Equis, Tecate) in Mexican and Canadian markets. Overall, expect continued strategic M&A: firms will prune non-core assets (like AB’s packaging sale) while acquiring craft/health-focused brands to capture growth niches.

Domestic Market Dynamics: Trade, Tariffs, and Consumer Shifts

Key domestic markets face their own pressures. In the U.S., beer import tariffs have upended trade flows. As of April 2025, the U.S. imposed a 25% tariff on all imported beer (bottled and canned). This hit Mexican imports hardest (Mexico was 83% of U.S. beer imports in 2024). Similarly, a 25% U.S. tariff on imported aluminum (from Canada and elsewhere) raised domestic can costs significantly. Beer distributors expect these tariffs to make once-cheap imports (Corona, Modelo, European lagers) more expensive, potentially driving shoppers toward U.S. brands. U.S. domestic brewers have lobbied for these tariffs, arguing they level the playing field for local producers. Conversely, countries like Canada and Mexico have retaliated: Canada slapped 25% duties on U.S. beer (as of March 2025) and Mexico added tariffs on U.S. goods (Aug 2025), creating complexity for exporters.

Consumers are shifting too. U.S. beer consumption is mature and even declining; the Brewers Association reports craft beer production fell 3.9% in 2024 (to 23.1 million barrels), and total U.S. beer volume declined about 1% that year. Young drinkers are choosing spirits, ready-to-drink cocktails, and non-alcoholic options over traditional lagers. A survey shows 84% of craft-drinkers want the convenience of brewery subscription clubs, indicating many prefer curated variety over volume. Added to this, the pandemic accelerated e-commerce and direct-to-consumer buying: AB InBev reports its digital platforms (BEES for retailers and delivery apps) drove record revenues in 2024.

For domestic beer producers, this means competing on value and innovation. U.S. breweries with solid supply chains (and no reliance on imported inputs) may gain share as imported options shrink. However, many craft and small brewers are squeezed by rising input costs: tariffs on stainless brewing equipment, steel kegs, aluminum cans, hops and malt have all climbed. Retailers, facing price pressure, are also rationalizing SKU counts (favoring core brands and cold classics). In response, domestic brewers are hiking prices and emphasizing local supply narratives (“buy American”) to retain customers.

Craft Beer: Consolidation and Innovation in a Mature Market

The craft segment is deep in consolidation. In 2024 the U.S. craft brewery count actually shrank: 9,736 craft breweries operated (down from ~10,000) as 399 closed and only 335 opened. This is the first time closures surpassed openings in modern history. Many small breweries simply couldn’t sustain inflationary costs or taproom sales dips. What remains are stronger (or more efficiently managed) operations. Some breweries merged or were acquired; for example, regional players in the U.K. like Keystone Brewing Group have rolled up struggling labels. Even in the U.S., groups like CANarchy (at one point) and beer-portfolios of large alcohol companies are consolidating craft brands to achieve scale.

Innovation, however, has not stopped. Craft brewers are refocusing on their core successes. The Brewers Association notes that surviving craft brewers are “doubling down on what works” - their flagship styles, popular IPAs, and local specialties - while cutting peripheral offerings. Taprooms have evolved: many now serve food, cocktails and non-beer drinks to broaden appeal (see the next section). New product launches are still common in niche areas: experimental sours, barrel-aged stouts, and heritage revivals (like lagering or old-world styles) attract dedicated fans.

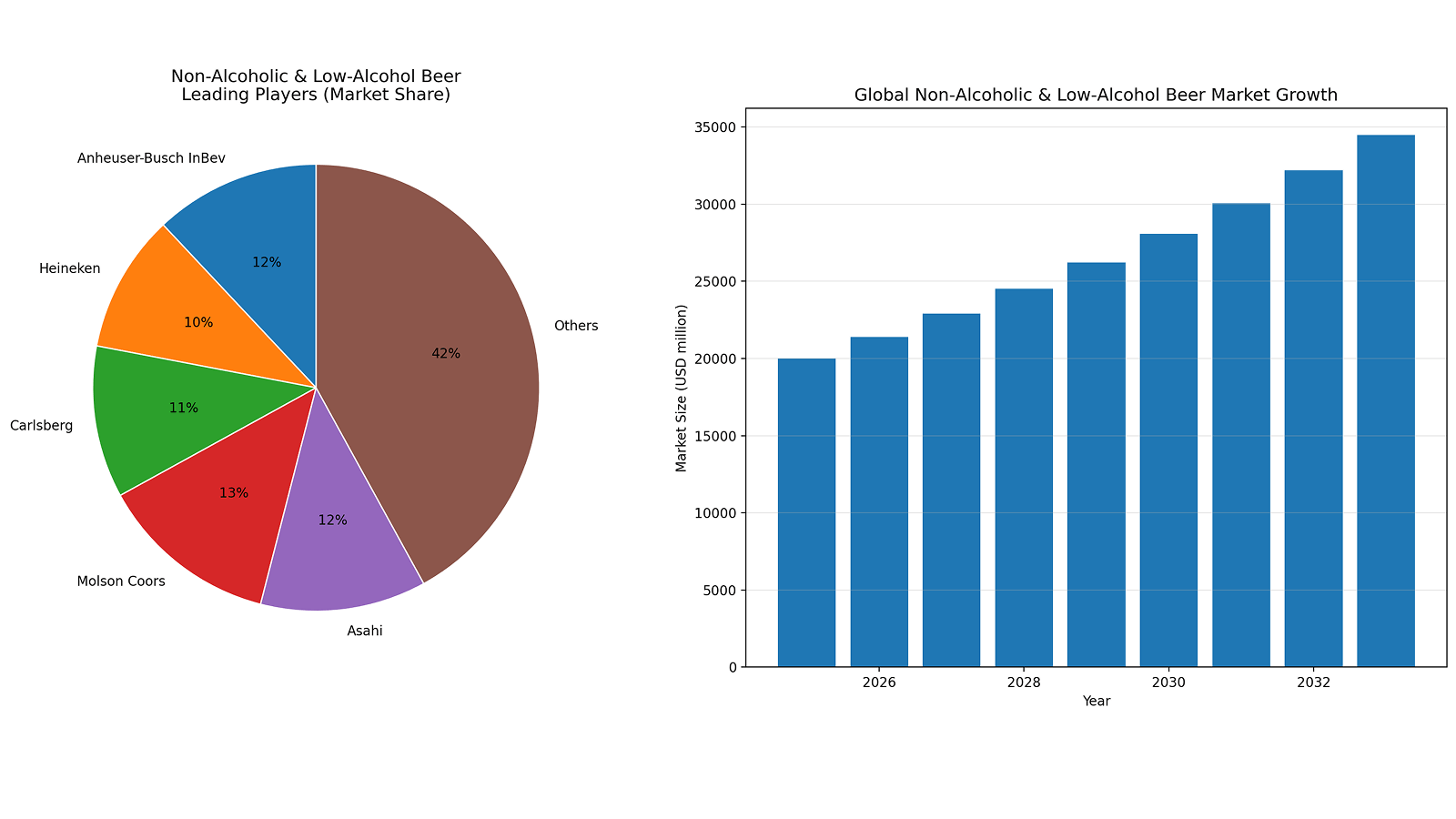

One bright spot: non-alcoholic beers. Among craft brewers, NA beer sales soared 30% year-over-year in early 2024. Nearly half of craft breweries now offer at least one non-alcoholic or low-ABV option, up from 8% a few years ago. Market leaders like Lucky Saint (UK) and Big Drop (UK), along with legacy brands like Bitburger NA (Germany), are gaining traction. Global brewers are investing heavily in this niche too - Budweiser, Heineken and AB InBev all have 0.0 portfolios, and joint ventures (e.g. Heineken’s Lagunitas Hi-Fi Hops) span craft-style cannabis drinks. In short, the craft beer world in 2026 is leaner and more competitive, but also nimble: breweries are crafting new experiences and beverages to stay relevant in a fuller beverage landscape.

Craft breweries are innovating even as the market matures - many now focus on taproom hospitality and core recipes, while introducing low-alcohol and craft-cocktail offerings.

Health and Wellness Beers: Low-ABV, Non-Alcoholic, and Functional Trends

Health-conscious drinking continues to reshape beer. Low-ABV “session” beers, non-alcoholic lagers, and “functional” craft brews are booming. According to industry data, U.S. NA beer sales jumped 111% by volume from 2021 to 2025, reflecting exploding interest. In craft beer specifically, January-October 2024 saw NA volumes rise 30% over the prior year. Consumers eager to socialize without overdoing calories or hangovers are trying “mindful” beers: low-carb IPAs, botanical-infused lagers, and even drinks with probiotics.

Some brewers are taking this further by adding functional ingredients. In Asia, one brewery’s SayPlay Cold IPA (with only 2.5g carbs) became the top-selling craft beer in Thailand, underscoring the low-carb trend. Researchers at Singapore’s National University developed a sour beer (Probicient Red) containing 1 billion probiotic CFUs per glass (while still tasting like a fruit ale). Though still niche, such products signal R&D directions: fiber-infused “gut-friendly” beers or adaptogenic (mushroom, herbal) brews could emerge in 2026.

Meanwhile, major brands are expanding their NA/low-ABV portfolios. Budweiser Zero (4.2% ABV) and Corona Cero saw double-digit growth in 2024. Heineken’s global 0.0 labels (Heineken 0.0, Desperados 0.0) continue strong. Millennial and Gen Z drinkers - especially women - are driving this, as surveys show they perceive cannabis and low-alcohol drinks as “healthier” choices. In practice, many consumers now alternate alcoholic beers with zero-proof drafts or “mocktails” at brewpubs. Brewers should therefore continue expanding low-alcohol lines and even exploring nutrient or botanical additions to appeal to wellness-minded customers.

Emerging Categories: Seltzers, Flavored Malt Drinks, and Cannabis-Infused Beverages

Several adjacent categories continue their impact:

- Hard Seltzers & RTDs: The malt-seltzer craze (2018-2021) has plateaued, but the category remains large. Newer entrants use spirits (vodka, tequila, mezcal) as bases, offering a more “authentic” cocktail-like experience. IWSR notes that vodka/tequila-based seltzers are growing faster than the original malt versions, since they feel more premium. Brands like Anheuser-Busch’s White Claw (tequila variant) and Diageo’s Smirnoff (vodka mix) exemplify this shift. Flavored malt drinks (hard iced teas, lemonades, punch drinks) are also steady sellers: volumes in this “cooler” segment are rising 5-10% as consumers seek sweeter, ready-mix options (BevIndustry 2025 report). The overall takeaway is that drinkers still crave novelty and convenience: convenient single-serve cans with diverse flavors remain a lucrative niche.

- Cannabis-Infused Beverages: This is the fastest-growing segment in alcohol-alternatives. U.S. sales of ready-to-drink THC beverages passed $1 billion in 2024, with analysts projecting $10-15 billion in a few years. Growth rates of 15-30% per year are reported in legal states (some even doubling year-over-year). These include hemp-derived THC seltzers and cannabis beers (with <0.5% THC in alcohol-distribution channels) as well as non-intoxicating CBD beers. Notably, the demographic for cannabis drinks overlaps heavily with craft beer enthusiasts: younger adults who want a buzz without the calories or hangover.

- Big beverage companies are moving swiftly: Constellation Brands invested heavily in Canada’s Canopy Growth for cannabis beers, and Molson Coors formed a joint venture (Hop Thing) to launch THC beverages. Heineken’s Lagunitas label debuted Hi-Fi Hops (a CBD/THC drink portfolio). In the U.S., shifting regulations (e.g. Minnesota now allows taprooms to serve hemp-based THC drinks) are opening mainstream channels. Brand owners should monitor this trend closely: some breweries have already started pilot projects or partnerships with cannabis producers. Even if regulations remain murky in some markets, offering CBD-infused non-alc beer or “light” cannabis beers may attract customers seeking a different kind of relaxation.

Sustainability: Eco-Friendly Brewing, Packaging, and ESG Initiatives

Environmental and social responsibility are rising imperatives. Consumers and retailers now expect green practices, and regulators are tightening waste and emissions rules. Many leading brewers have pledged net-zero carbon targets (often by 2040). For example, Carlsberg has committed to net-zero CO2 at all breweries by 2030 and in its full value chain by 2040. To meet this, Carlsberg (and others) is deploying biomass boilers, investing in solar/wind power, and shifting to 100% renewable electricity from new assets. Similarly, Heineken, AB InBev and Molson Coors each have set aggressive emission-reduction plans, often including electric delivery fleets and waste-heat reuse.

Water use is another focus: beer is ~95% water, and breweries now use advanced water-recycling (closed-loop) systems to cut usage. Industry reports note breweries have slashed water-per-barrel by up to 30% using new tech. Spent grains, hops and yeast are routinely upcycled into animal feed, compost or even textiles, closing the loop on brewery by-products.

Packaging is under reform. Globally, brewers are switching to eco-friendly materials: lightweight aluminum cans (with high recycled content) and returnable glass loops. Carlsberg collects about 76% of its bottles and cans through take-back schemes, the highest in the industry. It’s also introduced recyclable and biodegradable labels. Many breweries are experimenting with refillable growlers and kegs to minimize one-way disposables. Even pint glasses and cardboard point-of-sale displays are being made from recycled sources.

Overall, sustainability is no longer optional: it’s a brand differentiator. Consumers (especially younger drinkers) favor breweries that talk openly about ESG goals. Brands are responding with carbon-footprint labels on packaging and third-party certifications (e.g. B Corp for breweries). In 2026, expect continued innovation in green brewing - from solar-powered brewing houses to regenerative-hop farming - as companies compete on their environmental track record and cost savings from efficiency gains.

Brewing is becoming greener: many breweries now use solar energy and recycle 100% of their container packaging.

Digital Transformation: E-commerce, AI, and Tech-Driven Engagement

The beer industry is undergoing a digital revolution. Large brewers report that e-commerce and tech have become central growth engines. AB InBev, for example, saw its B2B platform BEES grow 57% in 2024 (to $2.5B GMV), processing 36 million orders. Its direct-to-consumer apps (drink delivery and home taps) generated $1.4B in 2024, up 9%. These systems allow precise data on buyer behavior, so brewers can adjust production daily. Smaller craft breweries are following suit: brewery management software now integrates point-of-sale, inventory and e-commerce, enabling taprooms to offer click-and-collect orders, membership sales, and even online merchandise.

AI and data analytics are taking root on the production floor. Many brewers now use smart sensors and automated controls throughout fermentation and packaging. These systems continuously monitor yeast activity, temperature and pH, catching deviations before off-flavors develop. In pilot projects, AI-guided systems have cut energy use by ~15% (through optimized heating and cooling schedules) and extended yeast reuse life, reducing waste. Software tools (e.g. IntelliBrew, BeerX AI) can simulate new recipes: by inputting parameters like local water chemistry and grain types, they predict aroma and bitterness profiles before a batch is brewed. This virtual R&D saves time and ingredients.

On the marketing side, digital data is equally powerful. Breweries use AI to forecast demand: by analyzing POS data, weather forecasts, and social media trends, they predict which styles will spike (for example, lighter ales in summer months or pumpkin beers in autumn). Customer engagement has also gone digital: interactive apps (Untappd, brewpub loyalty apps) track personal preferences and offer rewards points. Many breweries now send targeted offers via email or SMS to loyalty members. Even blockchain and NFTs have appeared - for instance, AB InBev tested a blockchain-based mobile ad campaign in early 2024 to verify digital ad performance.

In short, technology is enabling “data-driven brewing.” Breweries that embrace it can improve product consistency, cut costs, and create highly personalized consumer outreach. By 2026, expect every midsize brewery to have an e-commerce shop and CRM (customer relationship management) system in place, and larger players to be exploring machine learning for everything from supply chain logistics to dynamic pricing.

On-Premise Trends: Experiential Taprooms and Hospitality Innovation

As more drinking shifts at-home, bars and brewpubs must up their game. Taprooms are evolving into multipurpose hospitality venues. Many now emphasize food: craft breweries are hiring chefs, offering full menus and even hosting brunches or weddings. Mixed-drink options are expanding - it’s common to find cocktail menus or craft spirits bars alongside beer taps. According to industry observers, “taprooms will need to refocus on offerings beyond beer” - for example, mixing signature beer cocktails and visually striking drinks to create Instagram-worthy experiences. This caters to customers who want novelty and choice.

Family-friendliness and “third-place” culture remain priorities. Brewery taprooms often invite families with games, picnic areas and inclusive events (e.g. alcohol-free beer garden days or sober-run meetups). They host live music, trivia nights, yoga classes and art shows - anything to keep local patrons coming back. Digital tools like QR-code menus and contactless payment have become standard. Tech-driven attractions (like augmented-reality beer labels or virtual beer tastings via video chat) are also emerging, especially among large chains.

Beer tourism is another boon: craft regions (like Pacific Northwest, Colorado, Belgium’s Flanders) now draw travel devoted to brewery visits. In 2026, on-premise businesses should continue blending brewery tours with dining and entertainment. Creating community-centric taprooms - whether through loyalty punch cards, member-only events, or co-branded partnerships (e.g. brewpubs co-hosting with local gyms or theaters) - will keep on-premise vibrant.

Modern taprooms are blending craft beer with culinary and event experiences. Many brewpubs now feature full kitchens, cocktail bars and family-friendly spaces.

Policy and Regulation: Taxes, Labeling, and Alcohol Guidelines

2026 will see important regulatory shifts for beer. On taxation, governments are reassessing alcohol duties. The WHO’s 2025 Global Alcohol Tax Report finds that many countries still under-tax alcohol, and urges higher excise taxes (ideally indexed to inflation and tied to alcohol content) across all beverage types. If this advice is heeded, we could see incremental beer duty hikes in markets like Europe and Latin America, affecting price and consumer affordability. Some countries have already signaled tougher stances: for example, Indonesia plans to raise beer excise in 2026, and Canada is considering uniform taxation instead of provincial rates.

Labeling is undergoing a revolution. In January 2025 the U.S. TTB proposed mandatory “Alcohol Facts” panels on beer and wine labels, akin to a Nutrition Facts box. This would require listing calories, carbs and protein per serving, plus any allergens. The Brewers Association has pressed for exemptions or longer phase-ins, but companies should prepare for change. EU regulators are also discussing more food-like labeling (after recent mandatory origin-label rules for hops and barley). Brands should also note any new health-warning requirements: some countries are adding graphic or textual warnings about alcohol risks on containers.

Drinking guidelines are trending stricter. The new 2025-30 U.S. Dietary Guidelines state “less alcohol for better health” but notably removed the previous two-drink/one-drink limits per day for men/women. Instead, they focus on overall moderation and occasional abstinence periods. Similar nuance appears in Canada’s and Australia’s latest guidelines. This reflects debates in medical research about low-level drinking risks. Marketing in 2026 should thus emphasize “responsible enjoyment” and clearly communicate unit sizes. For example, breweries may voluntarily list standard drink counts (already common in Australia/New Zealand) or link to apps that track intake.

Finally, regulatory regimes for cannabis will affect beer-adjacent products. U.S. states are still patchwork on hemp-derived THC beverage rules, but growing access means more competition for beer. Brewers should watch evolving laws (e.g. FDA potentially moving to regulate hemp-CBD products). On the alcohol side, one emerging issue is advertising: some governments may clamp down on beer ads aimed at younger demographics, especially around esports and social media. Companies should ensure compliance programs are robust and stay engaged on policy (for instance, Breweries have joined coalitions calling for evidence-based alcohol guidelines).

Marketing Strategies: Storytelling, Digital Campaigns, and Loyalty Programs

Beer marketing in 2026 will continue to blend tradition with tech. Storytelling is key: consumers crave authentic narratives, whether it’s a family brewery’s founding tale or a community cause. Brands that highlight their origin, craftsmanship and people foster loyalty. For example, a craft IPA can be marketed as “made with Pacific Northwest hops by four friends from college,” giving it character beyond taste. Similarly, highlighting sustainability efforts (like “brewed on 100% solar energy”) can differentiate. Digital storytelling via short videos (brewery tours on YouTube, Instagram reels of pouring pints) engages younger drinkers.

Digital campaigns will leverage data. Influencer partnerships remain popular: a popular foodie Instagrammer or local sports figure enjoying your beer can sway brand awareness. Targeted social ads (e.g. Facebook/Instagram ads focusing on “beer lovers near Portland” or “college sports fans”) will be more data-driven thanks to broader privacy controls. Virtual events are another tactic - e.g. livestreamed tasting sessions or interactive webinars with the brewmaster. Email marketing tied to holidays (Oktoberfest promos, holiday gift packs) and to milestones (birthdays, anniversaries of sign-up) helps keep your brand top-of-mind.

Loyalty programs and e-commerce are no longer optional. Many breweries now operate beer clubs (monthly boxes, tiered memberships) that drive recurring revenue. Surveys show consumers love this model: 84% of craft fans are interested in buying direct via subscription. Breweries should simplify online ordering and consider rewards: points per purchase, referral bonuses, or exclusive member events. Untappd and other beer-rating apps offer emerging platforms for loyalty: check-ins can earn badges or discounts.

Crucially, marketers should ensure they link to multiple outlets when selling online. For example, if a beer is sold nationwide, provide links to several major retailers or delivery services (Amazon, Drizly, local liquor chains) so customers have options and competitive pricing. This aligns with best practices on discoverability and user value. Cross-promotion (e.g. including beer with food delivery menus, or bundling with brewing kits for homebrewers) can open new channels.

Focus on quality content and user value: share behind-the-scenes videos, provide brewing tips, or run a “meet the brewer” live Q&A. Invite user-generated content (photo contests of people enjoying your beer). Run loyalty surveys to adapt flavors or merchandise. The more a brewery operates like a lifestyle brand with genuine relationships, the stronger it will compete in 2026.

Key Recommendations for 2026 Success

- Capitalize on Major Events: Align marketing and supply plans with FIFA 2026 and other sports/pop culture events. Create fan-centric promotions and ensure ample supply of key brands.

- Innovate the Product Line: Expand low-/no-alcohol variants and premium RTDs. Invest in emerging drinks (hard seltzers, cannabis beverages, botanical beers) to capture health-conscious and younger segments.

- Embrace Sustainability: Accelerate green initiatives - renewable energy, waste reduction and recycled packaging - to reduce costs and appeal to eco-aware consumers. Publicize these efforts transparently.

- Leverage Digital & Data: Build robust e-commerce/DTC channels and CRM systems (as AB InBev’s BEES has done). Use AI and analytics for demand forecasting and quality control. Develop a loyalty/app strategy (beer clubs, points) to lock in repeat buyers.

- Enhance On-Premise Experiences: Turn taprooms into destinations. Offer compelling food & drink pairings, events and unique experiences (brewery tours, exclusive taps, beer-food festivals). Differentiate with cocktail menus or family amenities.

- Adapt to Policy Shifts: Monitor and plan for new tariffs and taxes. Adjust pricing or sourcing as needed. Prepare for labeling changes (nutrition/allergen facts on packs) and communicate responsibly under updated guidelines.

- Strengthen Brand Story and Loyalty: Craft a coherent brand narrative. Deploy engaging digital campaigns (social media, influencer, content marketing) that highlight what makes your brand unique. Build loyalty with subscription models and rewards (84% of drinkers crave subscription options). Ensure omnichannel presence (retail and online) for maximum reach.

Conclusion: Charting a New Course for Beer

The beer industry in 2026 will look quite different than in the past decade. Global events will momentarily spike demand, but long-term success will hinge on adaptability. Brewers must navigate trade headwinds and regulatory changes, while pivoting to where consumers are heading: premium flavors, wellness drinks, and engaging experiences. Those who innovate - whether through smarter brewing technologies, eco-friendly operations, or bold new products - will gain advantage. Meanwhile, powerful brands should remember that beer still thrives on community and storytelling: even as we embrace AI and e-commerce, the best marketing will always feel authentic and people-first. By balancing these forces, alcohol brand owners and marketers can ensure 2026 is not just a year of transition, but a turning point toward a stronger, more diverse beer future.

.svg)